Updated: May 09, 2024

If there’s anything that recent global events have taught us, it’s new and emerging risks can develop quicky, causing unprecedented damage and losses. Given the situation, insurers are pressed to come up with creative and innovative ways to offer clients adequate protection.

Enter parametric insurance.

This type of insurance product has been gaining traction around the world in recent years. It has been described by some industry experts as “an elegant solution for risk-transfer concerns.” It has also been lauded as an attractive alternative and enhancement to some traditional indemnity policies. But how does the policy work exactly?

In this article, Insurance Business digs deeper into this innovative insurance solution. We will discuss how parametric insurance works, what its pros and cons are, and what lies ahead for this fast-emerging insurance product.

This piece can prove useful for both industry professionals and insurance buyers wanting to learn more about this type of product. Read on and find out how parametric insurance can help address your coverage needs.

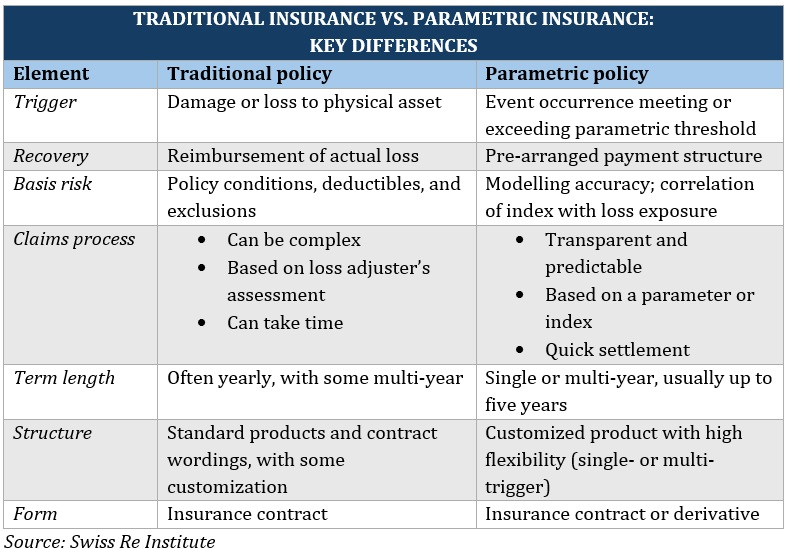

Parametric insurance is a type of policy that covers a predetermined set of conditions – also called parameters – instead of the actual losses. Under this arrangement, the insurer pays the policyholder a guaranteed amount once an agreed upon triggering event occurs.

“Parametric insurance works using a clearly defined parameter – i.e. a metric or an index that is easy to determine,” explains Steve Harry, senior vice-president at Marsh Risk Analytics. “Broadly, it’s an insurance program that is triggered, and/or paid very simply using an index rather than words.”

Also called index-based insurance, parametric policies consist of two key elements:

A triggering event is a set of predefined parameters for which a policyholder can receive compensation. To be considered as an insurable trigger, an event must happen by chance and can be measured objectively.

Some examples of triggering events include:

Coverage kicks in when the set conditions are met or surpassed. These conditions are then measured through an objective parameter or index related to the triggering event. The indices often come from an independent third-party source. This is done to avoid any potential conflict of interest and ensure data transparency.

Not all parametric insurance policies, however, are triggered by a single event. Some require multiple triggers before payouts can begin.

Here are some indices that parametric insurance providers use to measure insurable triggers.

|

Agency |

Parameter/index |

|

Australian Bureau of Meteorology (BoM) |

Tropical cyclone category |

|

Hong Kong Observatory (HKO) |

Typhoon warning signal |

|

Japan Meteorological Agency (JMA) |

Seismic intensity |

|

Singapore National Environmental Agency (NEA) |

Pollutant Standard Index (PSI) |

|

United States Geological Survey (USGS) |

Earthquake magnitude |

The insurer and the policyholder must have a pre-agreed payout amount if a certain index threshold is reached. This is regardless of the actual physical losses. For example, an insurance company and a construction business may agree on a $10-million payout if a magnitude 6.0 earthquake strikes a defined geographical area.

The index threshold is often set to align with the insured’s risk tolerance. In the parametric insurance example above, the business may have sufficient risk mitigation measures in place for a 5.0 to 5.9-magnitude earthquake. But for stronger magnitudes, the construction firm chose to get an alternative risk transfer solution in the form of parametric insurance.

One of the most interesting and attractive elements of a parametric solution is the faster insurance claims process.

Depending on the complexity, traditional indemnity claims may take months or even years to resolve. Compensation for a parametric policy, on the other hand, can be sent within four weeks once triggered.

Because parametric insurance doesn’t require loss adjustment, the payouts are given faster. The insurer can send the payment once the triggering event has been established and the index threshold is met.

Another prominent part of parametric insurance is basis risk. There’s a common misconception that this element exists only in this type of policy. Basis risk, however, is present in all types of insurance structures.

In traditional indemnity insurance, basis risk comes in the form of insurance deductibles, sub-limits, and policy exclusions. This can lead to a mismatch between the policyholder’s coverage expectations and the actual compensation paid under the policy.

In parametric insurance, basis risk happens when index measurements don’t align with the policyholder’s actual losses. While basis risk can’t be fully avoided, it can be lessened with the use of more complex parametric structures. These can include double trigger events and staggered payouts.

Parametric insurance is designed to fill the protection gaps left by traditional indemnity plans. Parametric policies, therefore, aren’t intended to be standalone solutions. Still, this type of coverage offers several advantages:

Parametric insurance offers fixed payouts based on the likelihood that a triggering event occurs. This allows insurance companies to calculate insurance premiums accurately and efficiently. This is important especially when dealing with low frequency but extreme events.

Parametric solutions also require less information from the policyholders. This and the fact that such policies are easier to price hasten the insurance underwriting process.

Basing payouts on predefined index thresholds allows quicker resolution of claims. Unlike traditional insurance in which the claims process can take months, parametric insurance payouts are often sent within 30 days. This enables businesses to recover faster from a loss.

Parametric insurance is designed to cater to different coverage needs. Insurance companies can offer customized coverage limits, conditions for compensation, and term lengths.

The speed and transparency that parametric policies bring allows insurers to build trust and loyalty through better customer service.

“Everything is predefined in the parametric insurance contract, and there’s no ambiguity over when, how, and how much the contracts are going to pay out,” explains Alex Kaplan, executive vice-president of alternative risk at Amwins Group, in a 2023 interview with Insurance Business.

“Often, people's biggest complaint about insurance is that it's too slow and it's too ambiguous. Parametric insurance serves to alleviate those two chief complaints.”

In a 2022 study, data analytics firm InsTech identified four key challenges facing the parametric insurance segment:

The study found a general lack of understanding from insurance buyers and some retail brokers about how parametric insurance works. The situation is prevalent for those who are used to buying or selling traditional indemnity policies.

Parametric insurance is generally seen as having a large basis risk. This can make such policies less enticing to clients.

Distribution and insurance capacity costs are typically higher in most parametric insurance products compared to those of conventional policies. These expenses have a direct impact on insurance premiums.

Because insurance laws are implemented with traditional indemnity insurance in mind, parametric solutions remain mostly unregulated. Fraud concerns are discouraging some customers from getting coverage. This is despite triggering events being based on third-party data, which makes fraudulent claims almost impossible.

Parametric insurance is designed to complement traditional insurance, not replace it. Parametric solutions can only be purchased as add-ons to a standalone policy. While adding this type of coverage to standard policies can raise your premiums, it can lower the total cost of risk if used correctly.

Parametric insurance is designed to fill the protection gaps left by traditional insurance. Someone whose policies come with very high insurance deductibles and multiple exclusions can benefit from a parametric solution.

“Buyers are now more sophisticated in the way that they look at their insurance, and they understand some of the limitations of a conventional insurance policy,” Harry notes. “Some people like the uncertainty that parametric insurance gives them, in that they can always argue about a policy contract, and other people like the certainty that an index-based product would give them.”

The scope of parametric insurance continues to grow. Initially, it only covered natural catastrophe risks. These include earthquakes and weather-related exposures. Parametric coverage has since expanded to non-physical damage such as business interruption losses.

A business owner might lose a certain amount of income over a period. This could trigger a payout without an identified event like a hurricane or flooding. This can open the possibilities of parametric insurance to more clients.

It’s another tool in their toolbox. An insurance broker's goal is to transfer as much of a client’s risk as possible to provide peace of mind and business and life continuity. Parametric insurance enables a broker to place a strong policy and enhance that by filling any coverage gaps. This, in turn, lets them offer a more holistic risk transfer service.

When considering parametric solutions, brokers need a deep understanding of their commercial client’s business model. The data demands of parametrics are more complex. It can also be more expensive because the cover tends to be wider.

“For risk managers [dealing with insurance brokers], taking the time to understand their firm’s ability to withstand future ‘shocks’ and gaining the support of the board are crucial first steps to incorporating parametric insurance solutions into their overall risk management strategy,” Harry says.

Before purchasing a parametric policy, brokers and their clients need a deep understanding of the loss exposures in play. They also need to consider the client’s economic ability to withstand future losses.

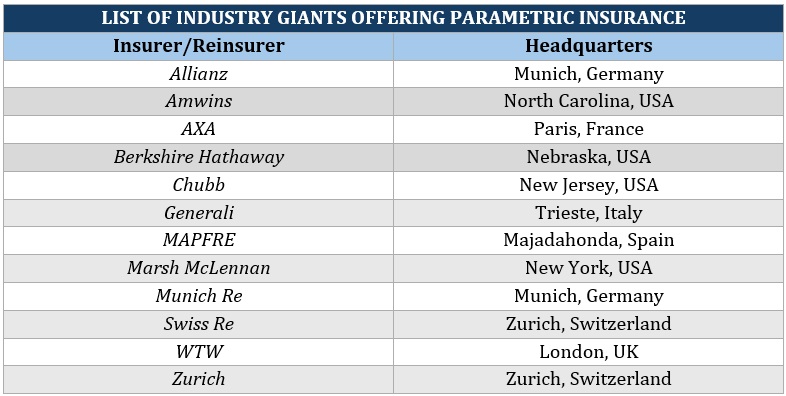

Many of the world’s largest insurance brands offer parametric solutions, including:

Here’s a list of some industry specialists offering parametric insurance solutions. The list is grouped by region. This includes industry players who offer auxiliary services such as data providers.

|

LIST OF PARAMETRIC INSURANCE PROVIDERS (UK & EUROPE) |

||

|

Company |

Specialty |

Headquarters |

|

Atekka |

Agricultural risks |

Paris, France |

|

blink parametric |

Business & travel risks |

Cork, Ireland |

|

CelsiusPro |

Climate risks & natural disasters |

Zurich, Switzerland |

|

Descartes Underwriting |

Climate risks |

Paris, France |

|

Eoliann |

Climate risks |

Turin, Italy |

|

Etherisc |

Blockchain insurance |

Munich, Germany |

|

Exante |

Predictive insurance |

Dublin, Ireland |

|

Fathom |

Water risks |

Bristol, UK |

|

FloodFlash |

Flood insurance |

London, UK |

|

Global Parametrics |

Disaster risk resilience |

London, UK |

|

IBISA |

Crop protection |

Luxembourg City, Luxembourg |

|

ICEYE |

Remote sensing solutions |

Espoo, Finland |

|

Insurwave |

Specialty insurance |

London, UK |

|

JBA Risk Management |

Flood risks |

Skipton, UK |

|

Kita |

Nature-based solutions |

Worcester, UK |

|

McKenzie Intelligence Services |

Commercial risks |

London, UK |

|

Meteo Protect |

Food risks |

Paris, France |

|

Moonshot Insurance |

Usage-based e-commerce insurance |

Paris, France |

|

Paratus |

Fuel & freight risks |

Saint Peter Port, Guernsey |

|

Perils |

Catastrophe insurance |

Zurich, Switzerland |

|

Previsico |

Flood insurance |

Loughborough, UK |

|

Riskwolf |

Digital risk |

Zurich, Switzerland |

|

Setoo |

Business continuity |

London, UK |

|

Skyline Partners |

Geospatial risk intelligence |

London, UK |

|

Speedwell Climate |

Climate risks |

St. Albans, UK |

|

UBIMET |

Weather forecasting |

Vienna, Austria |

|

VanderSat |

Satellite data for agriculture |

Haarlem, Netherlands |

|

Wetterheld.com |

Farm insurance |

Hamburg, Germany |

|

Yokahu |

Climate risks |

London, UK |

|

LIST OF PARAMETRIC INSURANCE PROVIDERS (UNITED STATES & CANADA) |

||

|

Company |

Specialty |

Headquarters |

|

Arbol |

Weather-related risks |

New York City, New York |

|

Air Worldwide |

Weather-related risks |

Boston, Massachusetts |

|

Athenium Analytics |

Weather-related risks |

Dover, New Hampshire |

|

Cape Analytics |

Property insurance |

Palo Alto, California |

|

CoreLogic |

Property & real estate solutions |

Irvine, California |

|

Cultovo |

Climate risks |

Toronto, Ontario |

|

Farmers Edge |

Agricultural risks |

Winnipeg, Manitoba |

|

Floodbase |

Flood risks |

New York City, New York |

|

Jumpstart Insurance |

Earthquake insurance |

Oakland, California |

|

Jupiter Intelligence |

Climate risks |

San Mateo, California |

|

Metabiota |

Infectious disease risks |

San Francisco, California |

|

New Paradigm Underwriters |

Supplemental windstorm insurance |

Fort Lauderdale, Florida |

|

OTONOMI |

Cargo insurance |

New York City, New York |

|

OTT Risk |

Business interruption insurance |

San Francisco, California |

|

QOMPLX |

Cyber risks |

Tysons, Virginia |

|

Parachute Insurance |

Weather-related risks |

Chicago, Illinois |

|

Parametrix |

Business continuity & cyber insurance |

New York City, New York |

|

Parsyl |

Cargo insurance |

Denver, Colorado |

|

Praedicat |

Emerging risk analytics |

Culver City, California |

|

RepTrak |

Corporate reputation management |

Boston, Massachusetts |

|

RMS |

Insurance-linked securities |

Newark, California |

|

Ryskex |

Alternative risks |

New York City, New York |

|

Safehub |

Catastrophe risk management |

San Francisco, California |

|

Stable |

Commodity risks |

New York City, New York |

|

The Demex Group |

Climate risks |

Washington, D.C. |

|

True Flood Risk |

Flood insurance |

Bronxville, New York |

|

Understory |

Climate risks |

Madison, Wisconsin |

|

WeatherFlow |

Weather-related risks |

Scotts Valley, California |

|

WorldCover |

Agricultural risks |

New York City, New York |

|

LIST OF PARAMETRIC INSURANCE PROVIDERS (REST OF THE WORLD) |

||

|

Company |

Specialty |

Headquarters |

|

African Risk Capacity |

Natural disaster & climate risks |

Johannesburg, South Africa |

|

Bounce Insurance |

Earthquake insurance |

Wellington, New Zealand |

|

CCRIF (Caribbean Catastrophe Risk Insurance Facility) |

Catastrophe risk insurance |

Grand Cayman, Cayman Islands |

|

FloodMapp |

Flood forecasting |

Brisbane, Australia |

|

GramCover |

Agricultural risks |

Noida, India |

|

Raincoat |

Natural disaster risks |

San Juan, Puerto Rico |

|

Reask |

Climate risk forecasting |

Sydney, Australia |

|

Super Seguros |

Simple insurance products for Latin America |

Mexico City, Mexico |

As risks evolve and policyholders look for more innovative and efficient ways to transfer their risk, parametric insurance products are expected to gain more traction in the future.

“Parametrics started to come in at much greater scale in advanced economies like the US simply because people realized the amount of total risk against what is insured is still very large,” Kaplan explains.

He adds that technological advancements have played an important role in improving the quality of data used in parametric insurance. He sees the increased use of remote sensing technology and satellite data to be among the key drivers of the segment’s evolution.

“With remote sensing technology, you have the ability to measure hail stone size, for example, or the velocity a hailstone hits a particular roof, or the depth of floodwaters in real time at a specific site,” Kaplan notes.

There is also the emergence of non-damage business interruption, allowing insurers to use economic performance metrics to measure risk.

Technology has played an essential role in the evolution of the insurance industry. If you want to find out which companies have made huge contributions to the sector’s innovation, you can check out our Best in Insurance Special Reports page where we unveiled the five-star winners of our Top Insurtech Companies awards. These firms have been nominated by their peers and vetted by our expert panel as dependable market leaders. These companies are recognized for driving creativity and innovation in the industry.

How do you see the future of parametric insurance? Do you think parametric solutions are truly a game-changer in the industry? Feel free to share your thoughts in the comments.