Insurance underwriters play a key role in safeguarding insurers from unnecessary financial losses. This makes the role an integral part of any insurance company.

If you’re considering a career in the insurance industry or simply want to know what an insurance underwriter does, you’ve come to the right place. In this article, we will explain the important contributions these professionals make in the insurance scheme of things. We will also discuss what it takes to become one and how the job differs from other roles in the industry.

An insurance underwriter is an industry professional tasked to determine whether an insurer can provide coverage to individuals, families, or businesses by evaluating the risks involved in insuring them. Underwriters work closely with other insurance professionals – such as actuaries, brokers, and risk managers – to craft ways on how insurance companies can strike a balance between providing competitive rates to attract and retain clients and maintaining profitability.

Insurance underwriters typically specialize in one insurance line. The most common of which are:

While the primary role of an insurance underwriter is to assess clients’ risk exposure to determine if they can be accepted for coverage, the scope of their roles goes beyond this.

The Bureau of Labor Statistics (BLS) has listed several duties and responsibilities that an insurance underwriter must perform. These include:

Insurance companies often prefer candidates with a bachelor’s degree to fill their insurance underwriter vacancies. Most insurers, however, also consider those with significant insurance-related work experience, even if they possess only an associate’s degree or a high school diploma. Insurance-related certifications can likewise help candidates land the job.

Here are the standard qualifications insurers are looking for when searching for potential insurance underwriters.

A bachelor’s degree in actuarial science, business, economics, finance, or mathematics provides a solid foundation for those looking to start a career as an insurance underwriter. They can also take insurance underwriting courses and other related programs at accredited colleges. Some universities offer master’s degrees in insurance risk management, which can open opportunities for career advancement.

Entry-level underwriters typically work under the supervision of a senior insurance writer for a certain period – usually 12 months – until they can perform their roles with minimal instruction. Some insurance companies also offer training programs to help new hires excel at their jobs.

Insurance underwriters are expected to obtain certification as they progress through their careers, especially if they are targeting a senior underwriter role or an underwriter management position. Each line offers a variety of underwriting certifications that keep insurance professionals updated about new products, regulatory changes, and the latest innovations.

Here are some examples of certifications that an insurance underwriter can take to help advance their careers:

Designed for professionals with at least two years of insurance underwriting experience, this consists of four core courses, three concentration courses, one elective course, and an ethics course. Underwriters must also pass an examination to be eligible for certification.

Offered by the American College of Financial Systems, this 18-month program is designed for those with at least three years of experience in the insurance industry. The curriculum consists of five core courses and three elective courses that cover a range of topics for life insurance professionals, including:

Candidates must likewise pass a test to earn a certificate.

This three-course program covers the basics of life insurance, risk management, investment products, and practice management. It is offered by the National Association of Insurance and Financial Advisors (NAIFA). Candidates are required to pass an exam to obtain certification.

Underwriters specializing in health insurance can complete the Registered Health Underwriter (RHU) certification from The American College, while business insurance underwriters can earn an Associate in Commercial Underwriting (AU) certification from the Insurance Institute of America.

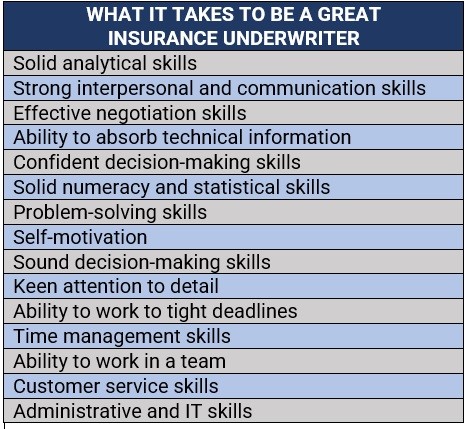

The five most essential skills that an insurance underwriter should possess to excel in their roles are:

Check out this special report if you want to get to know the industry’s most reliable and respected leaders. Our Leading Insurance Professionals in the USA list includes the country’s best insurance underwriters.

Most insurance underwriters work in the office full-time for the following businesses and organizations:

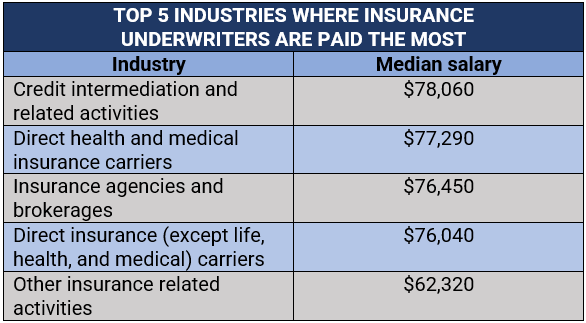

According to the most recent data from the BLS, insurance underwriters based in the US earn an average of $76,390 annually, with the lowest 10% earning less than $47,330 and the top 10% earning more than $126,380.

These are the top five industries where the median salaries for an insurance underwriter are the highest.

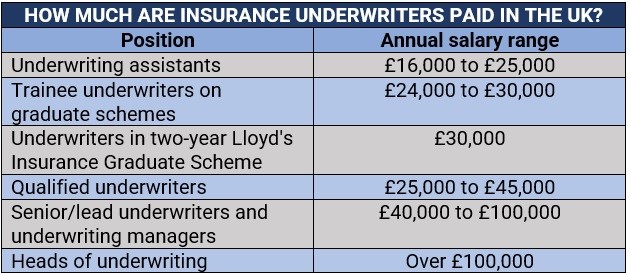

In the UK, the salary range for the different levels of insurance underwriters are as follows:

In Canada, the average insurance underwriter salary is CA$62,500 per year or CA$32.05 per hour. The salaries for entry-level positions start at $48,750 per year, while most experienced workers can earn up to CA$96,412 annually.

Find out which insurance jobs pay the most in our latest rankings.

Insurance underwriters and insurance brokers both play key roles in the insurance industry, helping clients access various types of coverage. These professionals, however, perform vastly different duties.

As discussed above, an insurance underwriter works for an insurance company, assessing the risks potential clients pose and deciding if they can be approved for coverage. Underwriters also use a range of metrics to determine premium pricing and the terms and conditions of coverage, bearing in mind the company’s ability to maintain profit.

The primary role of an insurance broker, meanwhile, is that of a middleperson. They act as intermediaries between the buyers and the insurance companies, with the goal of assisting individuals and businesses in finding policies that cater to their unique needs. These industry professionals can work independently or as part of an insurance brokerage firm.

So, while an insurance underwriter puts the interest of the insurance company first, an insurance broker serves the customers, helping them find the coverage that suits their needs and budget.

Does becoming an insurance broker sound like a better fit for you? You can learn more about what it takes to become a successful insurance broker by checking out this article.

Insurance underwriting can be a challenging job. Underwriters are under constant pressure to attract and retain clients while helping insurers maintain profitability – two goals that often come into conflict with each other, especially in a highly competitive market. But with the right mix of technical ability and soft skills, industry professionals can excel in this role.

The table below lists the different attributes an insurance underwriter should have to become successful in this field.

If working for an insurer is not for you and you would rather start your own insurance company, this handy guide can give you a good head start.

For those seeking specialized insurance roles such as insurance underwriter, there are several industry-specific job search websites for insurance jobs in the US available.

In addition to job search websites, there are also staffing agencies that specialize in placing candidates in insurance roles. These agencies can provide valuable guidance and support throughout the job search process, including resume writing and interview coaching.

Finally, job fairs and industry events can be a valuable way to connect with potential employers and learn about job opportunities in the insurance industry. Many insurance companies participate in these events to recruit new talent and raise awareness about their brand and culture.

The short answer is yes. The US Bureau of Labor Statistics revealed that the median pay of an insurance underwriter is around $36.73 per hour, or $76,390 a year, as of 2021.

Top-performing senior insurance underwriters can earn up to $182,500 a year.

Given that the minimum wage is still pegged at $7.25 an hour, insurance underwriters can and usually do make a lot of money.

First, it helps to have the right work ethic and the right set of skills.

An underwriter needs to have excellent interpersonal and communication skills to succeed, since the job can require talking to all sorts of people.

Excellent math skills are essential, as the job calls for calculating risk and making exact computations for them.

Problem-solving, decision-making, and analytical skills are likewise important, since you may have to deal with credit applications, IPOs, debt ratios and other financial concepts.

Being tech-savvy is also important, as most of the filing, communicating and paperwork is done with apps and software programs nowadays.

It can also help to be active on social media and know your way around data, as one insurance company CEO suggested.

Underwriters usually work regular office hours. On occasion, some insurance underwriters may be required to work overtime or on weekends, if they have deadlines.

Simply put, yes, underwriting can be a stressful job. It can involve a lot of responsibility, and the underwriter must have the ability to make quick decisions based on facts. An underwriter must objectively assess risks, then come up with the best rates for the insurance company and the insured.

The job also requires that the underwriter be highly familiar with insurance regulations, risk management, risk assessment, and finance.

To be a successful and respected underwriter, you’ll need a strong work ethic. This means being organized and methodical in your work while being able to meet tight deadlines.

The term “underwriting” was believed to refer to the practice of one of the world’s oldest insurers, Lloyd’s of London.

The company would accept part of the possible cost of an event’s risk in exchange for a premium. At that time – the early stages of the industrial revolution – individuals paying premiums to mitigate losses would write their names under the description of the property or event that Lloyd’s was assuming part of the risk for. This gave rise to the terms “written under” or “underwriting”.

The personality of a successful insurance underwriter is one who has integrity, great at analytical thinking, and has meticulous attention to detail.

A good insurance underwriter must be honest, ethical, detail-oriented and rigorous at performing their work.

Although you don’t typically need a degree to become an underwriter as there is no formal course or specific university degrees for underwriters, it’s better to get one. A bachelor’s degree can help you become reasonably good at math, analytical thinking, business, and finance – all useful to underwriters.

Good communication and writing well are also important, and studying for a bachelor’s degree can help you develop these essential skills. You might find it more difficult to start out as an insurance underwriter without a degree, as you could lose opportunities to job applicants who have them.

Some of the best degrees are those that can familiarize you with the skills, concepts, and regulations you’ll need to know and apply as an underwriter.

Viable degrees include business, accounting, finance, economics, and other similarly related degrees. If you already have a degree that may not be related to insurance underwriting, you can take a Master of Business Administration to learn the essential knowledge and skills.

Any degree or course that can build on your tech skills is also useful, as you might use hi-tech tools as you do underwriting work.

On average, it can take about 6 months to a year of on-the-job training to become an underwriter. This can involve getting an internship and having the aspiring underwriter train under a more experienced insurance underwriter.

Technically, it can take four to five years, if you count the time it takes to get a bachelor’s degree.

Most underwriters start off as a trainee or assistant underwriter. Some companies may hire fresh grads as entry-level underwriters, but it’s not unusual for other companies to prefer people with some previous underwriting experience.

If you’re hired as a trainee or assistant underwriter, expect to work under a senior underwriter to learn the ropes.

As you gain more experience, the company will likely help you obtain certifications. For this, you will have to take special courses and exams.

When you gain even more experience, it’s likely that you’ll be promoted to senior underwriter then eventually chief underwriter – but that will largely depend on your performance.

Do you think being an insurance underwriter is a good career option? Tell us why or why not in the comments section below.