Integration, Connectivity & Middleware

All systems go

Integration, connectivity, and middleware have become foundational components of the modern insurance industry. As insurers continue to evolve from legacy-based, siloed systems toward more digital and customer-centric operating models, the ability to connect systems, data, partners, and platforms seamlessly is now a business necessity rather than a technical advantage.

From underwriting and policy administration to claims management and customer experience, insurers rely on a complex ecosystem of internal applications, third-party providers, brokers, MGAs, and digital platforms. Integration and connectivity enable these systems to exchange data efficiently, automate workflows, and support real-time decision-making, while middleware acts as the technology layer that orchestrates and manages interactions behind the scenes. And, as we head further into 2026, this sector is bigger, better, and bolder than ever before.

The state of legacy modernization

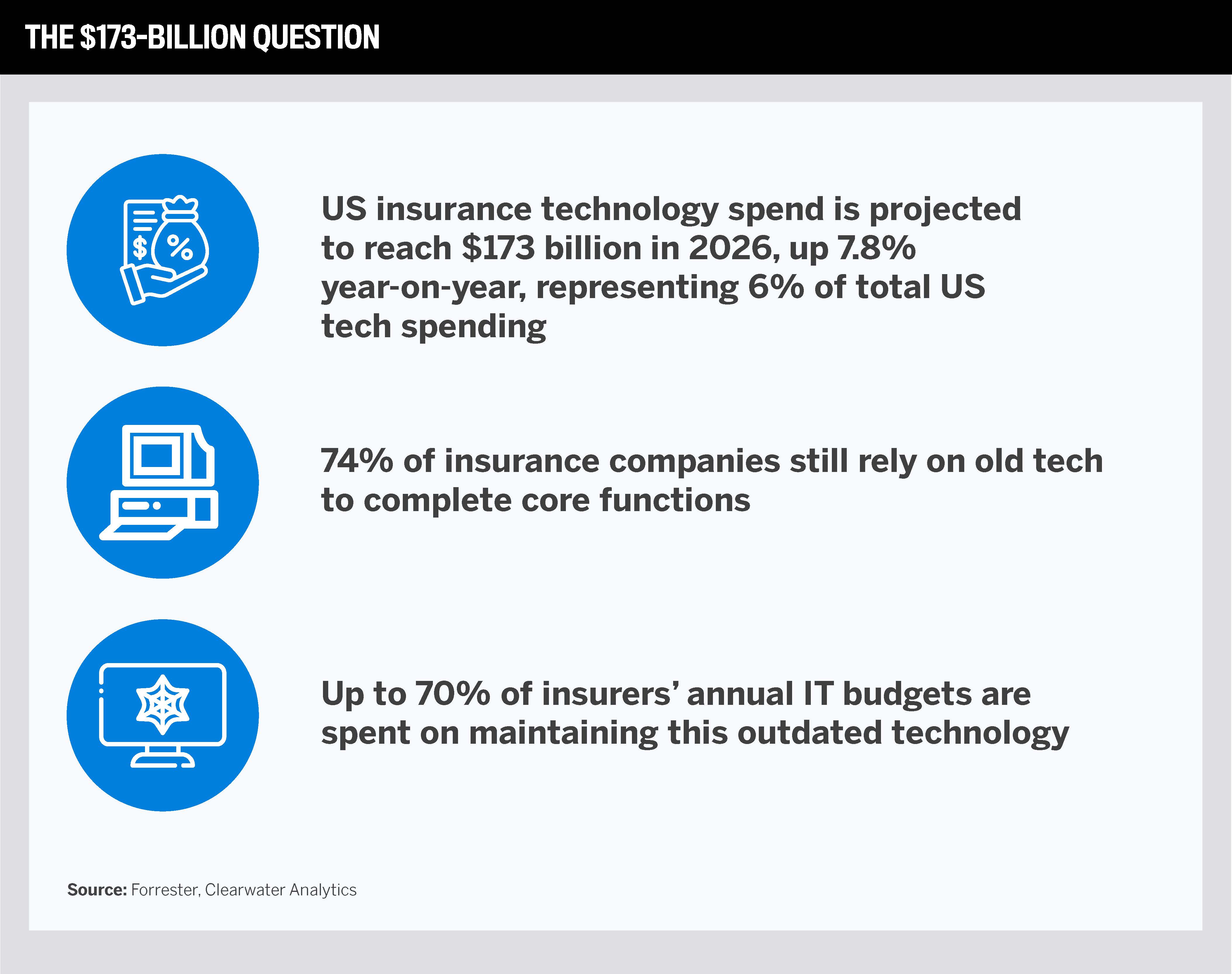

According to Forrester’s US Tech Forecast 2026, US insurance IT spending is projected to total $173 billion in 2026, up 7.8 percent on last year. Despite the uptick, many insurers continue to operate on legacy tech platforms – ones built decades ago to support key functions. And while these systems remain critical to day-to-day operations, they’re often difficult to scale, costly to maintain, and unable to support the digital experiences expected in today’s market.

As a result, legacy modernization has become a major strategic priority across the insurance sector. Insurers are increasingly looking to modernize their platforms without disrupting core operations or compromising business continuity, so much so that insurance alone will represent six percent of US total tech spending in 2026.

To avoid mass disruption, rather than replacing entire systems at once, many organizations are adopting phased transformation approaches that allow modern platforms and services to be introduced gradually alongside existing infrastructure.

The end goal? Systems that are holistic, connected, and seamless from the beginning of the process to its close.

“When systems are connected and routine work is automated, organizations can handle more volume, support new programs, and adapt to changing business needs without adding the same level of operational strain or internal headcount,” says Yuvaraj Selvaraj, senior director of product & strategic account management at EOX Vantage. “In that way, integration is not just a technical advantage, it creates a more flexible foundation for growth.”

Middleware in focus

Despite the desire to fully update these legacy models, a report from Clearwater Analytics reveals that as much as 74 percent of insurance companies still rely on old tech to complete core functions. Furthermore, up to 70 percent of insurers’ annual IT budgets are spent on maintaining this outdated technology. This is where middleware comes in. Middleware is fast becoming a core strategic area of investment for insurers in 2026, driven by these real-time changes in legacy systems.

“In insurance, organizations often rely on a mix of legacy platforms, PDFs, forms, spreadsheets, email, and manual processes,” adds Selvaraj. “In those environments, the challenge is usually not a lack of technology, but the fact that key information is scattered across systems that do not communicate well with one another.”

At EOX Vantage, they’ve solved this industry-wide problem through their innovation Taruvi platform, which creates a connective layer around the existing infrastructure. It centralizes operations, supports real-time dashboards and alerts, and gives teams role-specific visibility into submissions, SLAs, policy activity, compliance, and other operational metrics.

Yuvaraj SelvarajSenior Director of Product & Strategic Account Management,

EOX Vantage

API-driven insurance ecosystems, telematics integrations

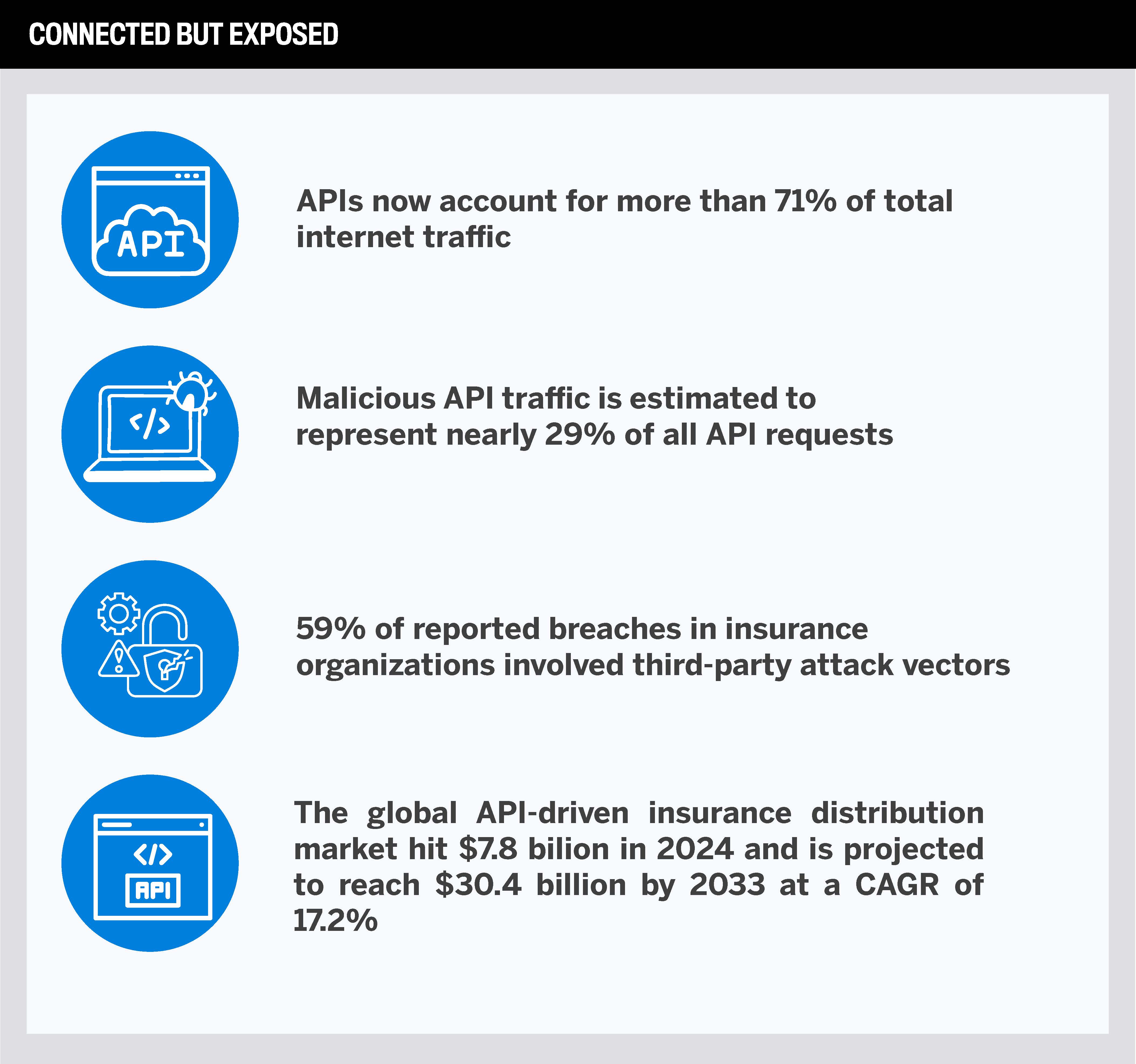

Application programming interfaces (APIs) are playing another key role in the evolution of modern insurance ecosystems this year, with the global API-driven insurance distribution market peaking at $7.8 billion in 2024 and projected to grow at a CAGR of 17.2 percent through 2033 to reach $30.4 billion. APIs enable insurers to connect systems, applications, and external partners in a secure and scalable way, allowing data and services to be exchanged in real time across the insurance value chain.

While traditionally, many insurers relied on tightly coupled systems and manual data exchange processes, which often limited agility and slowed collaboration with external partners, this year we’ve seen API-driven architectures helping to change this by creating more flexible environments.

Real-time data connectivity is also becoming a major competitive differentiator for insurers in 2026, enabling faster decision-making and improved customer experiences. As insurers continue to modernize their technology, the ability to access and process data instantly across systems and external sources is also reshaping core operations.

“The insurance industry is shifting from reactive operations to continuous, real-time decision-making,” explains Selvaraj. “Insurers are under increasing pressure to respond faster to customer needs, assess risk dynamically, and improve operational efficiency – all while managing growing regulatory and market complexity.

“One of the biggest trends is the move toward connected data ecosystems. Carriers are integrating internal systems with external data sources, such as telematics, IoT devices, third-party risk feeds, financial data, and behavioural insights to create a more complete, real-time view of risk and customer activity. That is enabling faster underwriting decisions, more responsive claims management, improved fraud detection, and increasingly personalized customer experiences.”

One of the most significant trends observed is the growth of real-time underwriting. Average claims processing time has dropped to 36 hours among AI-enabled insurers, down from 10 days in legacy systems. Insurers are now looking to integrate external data sources – including telematics, geospatial data, credit information, property intelligence, and IoT devices – directly into underwriting workflows.

“We are also seeing a growing emphasis on operational agility,” Selvaraj emphasizes. “Insurance organizations no longer want insights delivered days or weeks later through static reporting. They want real-time visibility that allows teams to act immediately, whether that is identifying fraud anomalies, monitoring claims trends, responding to catastrophic events, or surfacing underwriting risks as they emerge.”

At the same time, many insurers are realizing that speed alone is not enough. The quality, accessibility, and connectivity of data are becoming just as important as the analytics layer itself. Organizations that can unify fragmented systems and operationalize data across the enterprise are gaining a significant competitive advantage.

“Another emerging trend is the rise of AI-managed services,” Selvaraj says. “Many insurers want to leverage AI and automation, but do not necessarily want the burden of building and maintaining complex AI ecosystems internally. As a result, there is growing interest in managed models that combine AI-driven insights, workflow automation, integration support, and ongoing optimization services. This allows insurers to accelerate innovation while reducing operational strain on internal teams.”

What’s more, globally in 2026, usage-based, AI-auto insurance continues to expand through connected vehicle and telematics integrations. The telematics insurance market is estimated at 278.41 million active premiums in 2026, up from 216.07 million in 2025, and is projected to reach 988.8 million by 2031 at a CAGR of 28.85%.

Malware and cyber threats targeting integration layers

However, with every advantage innovative tech offers insurers, it gives the same ‘leg up’ to criminals. As insurers become increasingly connected through APIs, middleware platforms, cloud services, and third-party ecosystems, integration layers are emerging as a growing focus for threat actors in 2026. APIs now account for more than 71 percent of total internet traffic, making them the dominant communication layer across digital services and enterprise platforms. At the same time, malicious API traffic is estimated to represent nearly 29 percent of all API requests, making the case for good cyber hygiene even more essential in the years to come.

For insurers, this risk is particularly significant. Modern insurance operations rely heavily on interconnected systems to exchange sensitive customer, underwriting, claims, and financial data in real time. APIs and cloud integration platforms often sit at the center of these interactions, making them attractive targets for ransomware groups and supply chain attacks.

At the same time, threat actor tactics are also evolving. Rather than deploying malicious software, attackers are increasingly targeting identity systems, OAuth tokens, cloud platforms, and trusted third-party services to gain legitimate access to interconnected environments.

This trend is particularly relevant for insurers where ecosystem connectivity continues to expand through MGAs and external data providers, as supported by a recent study of insurance organizations, which found that 59 percent of reported breaches involved third-party attack vectors.

Yuvaraj SelvarajSenior Director of Product & Strategic Account Management,

EOX Vantage

AI and automation riding on connectivity

And when it comes to discussing digital security and cyber coverage, the topic of AI inevitably rears its head. While AI continues to dominate transformation strategies across the industry, the ability to move data efficiently between systems is what ultimately enables these technologies to operate effectively at scale.

This shift is becoming more pronounced as insurers move toward more autonomous and AI-driven operating models. According to the 2026 MuleSoft Connectivity Benchmark Report, 96 percent of IT leaders believe the success of AI agents depends heavily on seamless, debt-free data integration, while 86 percent warn that poorly integrated AI environments create more complexity than value. Despite this, the same research found that 50 percent of AI agents operate in isolation, outside of cohesive multi-agent systems and just 54 percent of organizations have a framework for centralized governance, necessary to ensure reliability and security.

“AI and automation are becoming foundational across the insurance industry, but their effectiveness depends entirely on the strength of the underlying integration infrastructure,” adds Selvaraj. “There is a growing recognition that AI is not simply a standalone tool layered on top of existing operations. It requires connected systems, accessible data, and seamless interoperability across platforms. Without that foundation, even the most advanced AI initiatives struggle to scale or deliver meaningful business value.”

Today, AI models and automated workflows rely on continuous access to real-time, high-quality data from across the insurance ecosystem. This includes information flowing between policy administration systems, claims platforms, customer applications, broker portals, cloud services, and third-party data providers. And without strong integration capabilities, insurers risk creating disconnected AI solutions that struggle to deliver meaningful operational value.

However, it’s not all been plain sailing. McKinsey’s State of AI Survey found that while almost nine in 10 organizations are experimenting with or using AI, the vast majority remain stuck in isolated pilots rather than seeing true scaled, enterprise-wide transformation – meaning there’s much more work to be done in 2027 and beyond.

The state of play: a glimpse ahead

In 2026, integration, connectivity, and middleware aren’t merely the background of the insurance industry. They have risen to become foundational to how insurers modernize, compete, innovate, and manage risk.

For insurers, the challenge is no longer simply connecting systems. It is about building resilient, scalable, and governed connectivity architectures capable of supporting the next generation of insurance operations.

“Ultimately, the future of AI in insurance is not just about intelligence,” adds Selvaraj. “It is about connectivity, orchestration, and operational scalability. The organizations that succeed will be the ones that build strong digital foundations capable of supporting real-time data exchange, intelligent automation, and agile decision-making across the enterprise.”

Keep up with the latest news and events

Join our mailing list, it’s free!