Top Cyber Insurance Companies in Canada |

5-Star Cyber

Jump to winners | Jump to methodology

Built for the breach

Among the top cyber insurance companies in Canada, the leaders are pulling ahead on response – uniting embedded technology, specialist teams, and coordinated claims models to manage complex incidents

The best cyber insurance companies in Canada: why this report matters

Canada’s cyber insurance industry has entered an exacting phase, with market growth matched by closer scrutiny of policy performance. Businesses of every size – from sole proprietors in Halifax to multinationals headquartered in Toronto – are discovering that the question is no longer whether to buy cyber coverage but which of the top cyber insurance companies in Canada can actually perform when an incident unfolds.

Data theft is overtaking ransomware as the defining loss event, AI is compressing attack timelines from weeks to hours, and shared vendors and cloud platforms are widening the blast radius of single incidents. These developments are pushing Canadian businesses to treat cyber risk as a measurable financial exposure that demands rigorous insurance rather than a discretionary add-on.

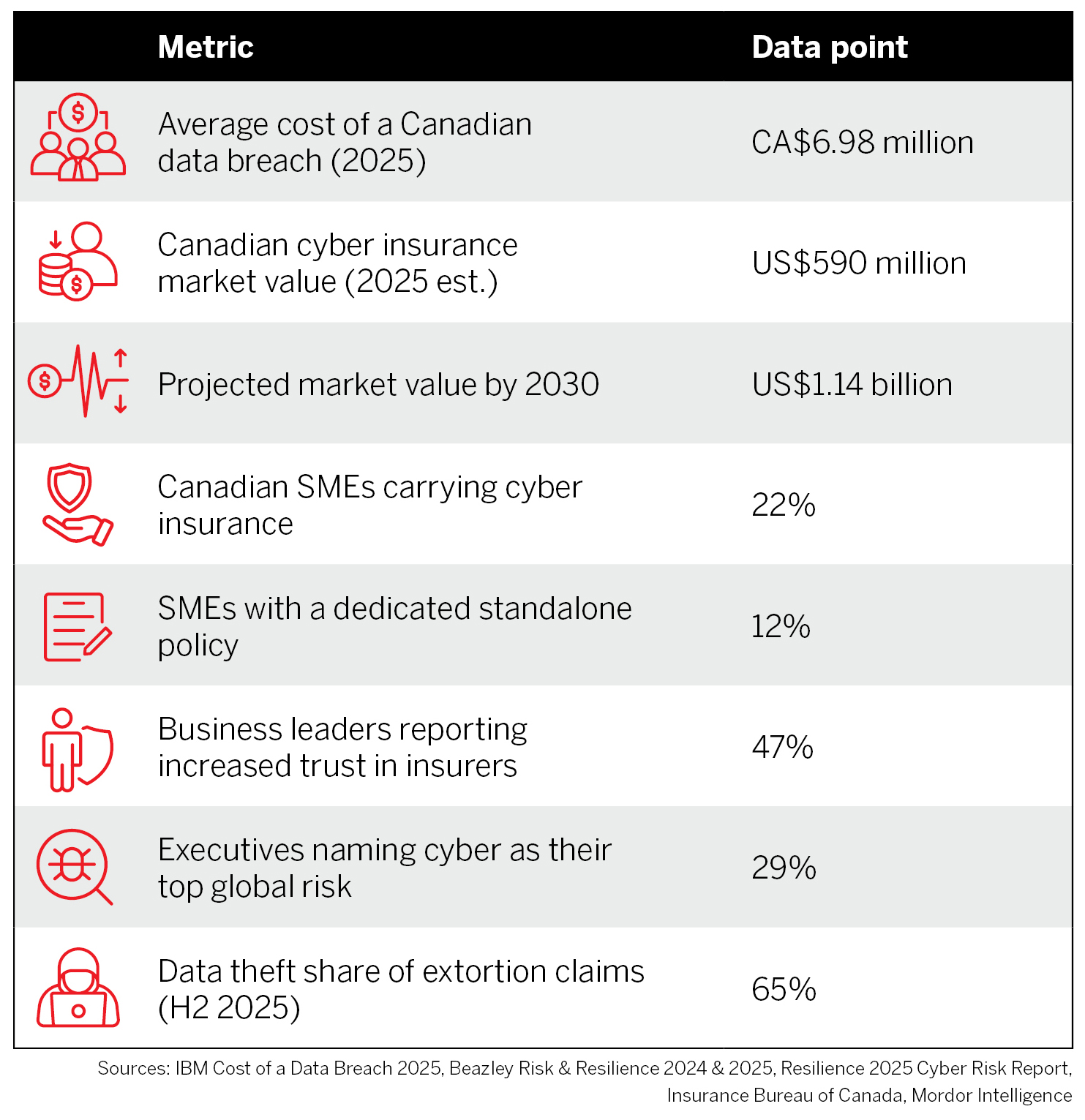

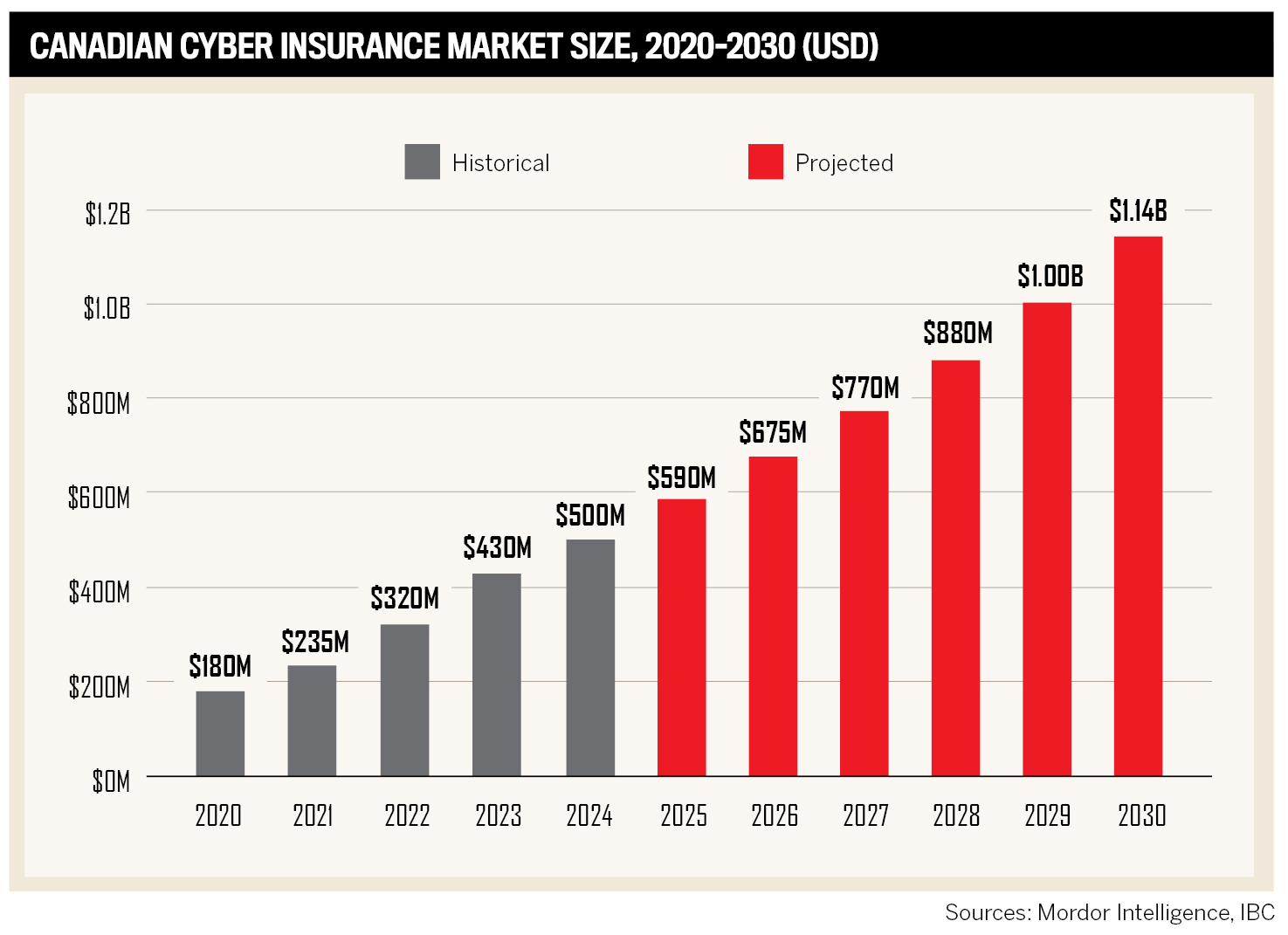

Industry analysis projects the Canadian cyber insurance market will surpass US$590 million in 2025 and reach US$1.14 billion by 2030, growing at a compound annual rate of approximately 14 percent. Yet rapid expansion has also raised the bar: brokers and buyers are examining not only what a policy covers but also how a carrier performs during the critical first 72 hours of an incident.

This report – produced through broker research and detailed insurer submissions by Insurance Business Canada – identifies the best cyber insurance companies in Canada for 2026. It examines how they are built, how they respond, and why their approach to underwriting, claims, and technology is setting a new performance standard for the market.

The evolving threat landscape shaping Canada’s cyber insurance market

The cyber risk environment that Canadian businesses face in 2026 is structurally different from that of three years ago.

According to Resilience data:

-

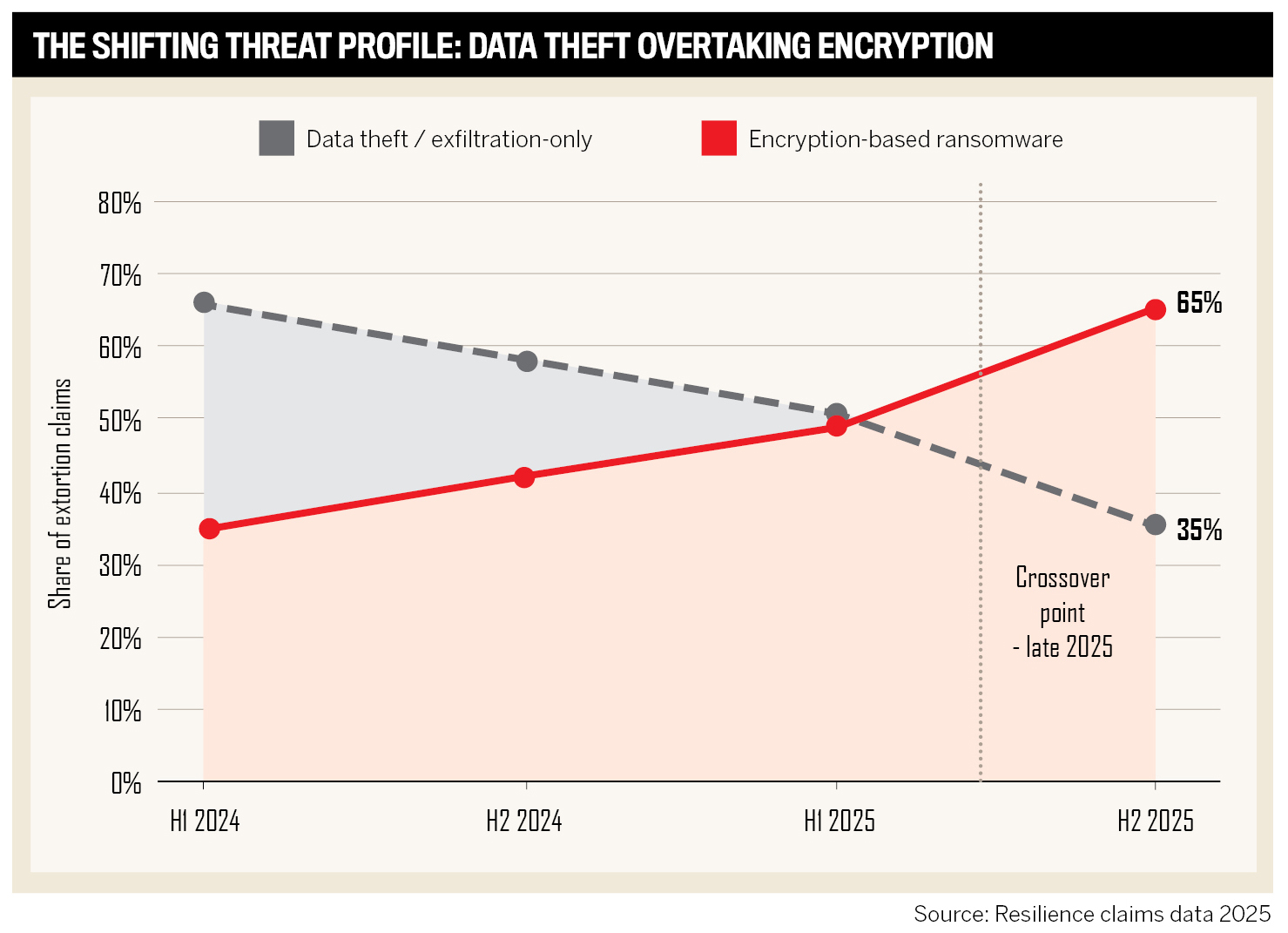

Ransomware, once the defining event insurers and brokers planned for, is no longer the primary measure of exposure.

-

Data theft without encryption now accounts for 65 percent of extortion claims in the second half of 2025, up from 49 percent in the first half of the same year

Attackers no longer need to lock systems to extract value; exfiltration alone carries sufficient leverage.

Canada's insured catastrophe losses by year

2024 shattered all previous records — $9.1 billion in full-year insured catastrophic losses, revised upward from the initial $8.5B estimate as individual event figures were updated through 2025 (CatIQ, January 2026). Four events in 27 days accounted for more than $8 billion of that total.

Sources: CatIQ, January 2025 (initial estimate); CatIQ, January 2026 (revised full-year 2024 total of $9.1B); Insurance Bureau of Canada. Figures in CAD billions. The 2024 figure reflects CatIQ's most recent full-year total as of January 2026, revised upward from the initial $8.5B estimate as individual event loss figures were updated.

Summer 2024 — Canada's four catastrophic events

In less than five weeks, four consecutive disasters produced Canada's costliest insurance season on record, generating over a quarter of a million claims.

July 15 — Toronto flooding | July 22 — Jasper wildfire | Aug 5 — Calgary hailstorm | Aug 9 — Hurricane Debby remnants

Sources: CatIQ one-year loss estimates (August 2025); Insurance Bureau of Canada In Brief report, "2024 Summer of Catastrophe across Canada" (October 2025).

Cyber claims —

ransomware demand and resistance trends

Ransomware actors are demanding more — but insured businesses are increasingly refusing to pay,

pointing to improved resilience and carrier-supported incident response.

Sources: Coalition 2026 Cyber Claims Report (March 2026); Coalition 2025 Cyber Claims Report (May 2025). Canada-specific average loss data from Coalition / SC Media, May 2025.

Insurance CEO AI investment priorities — KPMG 2025 survey

Based on 110 insurance CEOs globally (life, non-life, reinsurance, and broking). AI is reshaping claims, underwriting, and customer experience — and Canada's insurers are leading the sector's adoption curve.

Sources: KPMG 2025 Insurance CEO Outlook, KPMG International (January 2026) — 110 insurance CEOs surveyed. Canadian Chamber of Commerce Business Data Lab, Business Insights Quarterly Q4 2025. Insurance Business Canada (February 2026).

Northbridge Insurance — claims service performance

Northbridge's commercial P&C claims model is built around speed, specialist assignment, and field-level resolution capability — with measurable service standards across its national network.

Source: Northbridge Insurance insurer submission, IBC 5-Star Claims 2026 research process. Industry contact benchmark from BrokerLink / Reuters (December 2025).

IBC 5-Star Claims 2026 · Broker guide

Five questions to ask a carrier before a loss occurs

Choosing a claims carrier before a loss is the only time you have full negotiating leverage. These are the questions brokers and risk managers consistently wish they had asked earlier.

What are your documented service standards for first contact and adjuster assignment?

Verbal commitments don't tell you what happens when a CAT event hits and every adjuster is stretched. Ask for the written standard and ask how it held up in 2024 — Canada's costliest catastrophe year on record.

Do you have adjusters with specific expertise in the lines I'm placing?

Generalist handling on a complex cyber or commercial liability file carries real risk. Find out whether your file will be assigned to a specialist or whoever is available when the claim lands.

How do you handle coverage ambiguity?

The carriers that consistently earn the strongest broker ratings lean toward the insured's position when policy language is unclear. Ask directly what the carrier's philosophy is — and ask for a real example.

How will you keep me informed as my client's broker throughout the file?

Brokers who have to chase for updates are managing a client relationship breakdown that wasn't their fault. The best carriers treat broker communication as a structured responsibility, not an occasional courtesy.

How did your operation perform during the summer 2024 catastrophe events?

Canada's 2024 catastrophe season generated $9.1 billion in insured losses — the highest on record. How a carrier performed under that pressure, and what it structurally changed as a result, is more revealing than any service standard document.

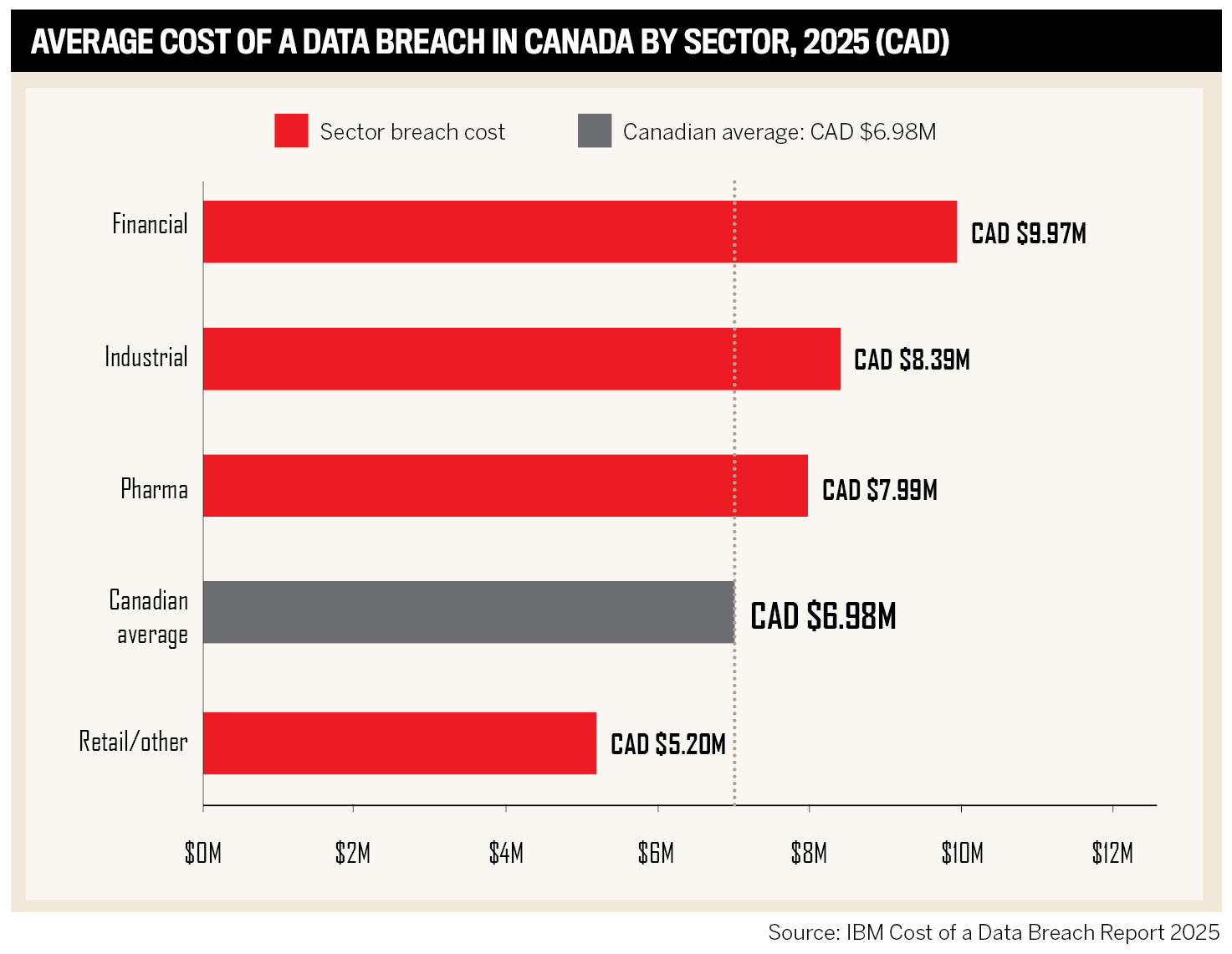

The IBM Cost of a Data Breach report found that the average cost of resolving a data breach in Canada reached CA$6.98 million in 2025. Phishing remains the most expensive vector, costing Canadian organizations an average of $7.91 million per breach – a 24 percent increase from $6.38 million in 2024. The financial sector leads all industries at $9.97 million per breach, with the industrial sector close behind at $8.39 million.

Shadow AI – the informal use of AI tools by employees without organizational oversight – is adding an estimated $308,000 per breach for Canadian businesses, reflecting how technology adoption is outpacing security governance. Globally, 29 percent of executives now name cyber as their top risk, the first increase since 2021, according to the Beazley Risk & Resilience 2025 report.

Aaron AanensonKYND

The Canadian Centre for Cyber Security projects ransomware will remain the leading threat to critical infrastructure through 2026. Bill C-8 – Canada’s critical infrastructure cybersecurity legislation, reintroduced in June 2025 to replace Bill C-26, which died on the order paper and which passed the House of Commons in March 2026 and is now before the Senate – is accelerating uptake among energy, utilities, and transport operators, with that segment advancing at an 18.6 percent compound annual rate.

Top Cyber Insurance Companies in Canada | 5-Star Cyber

- Aviva Canada

- Beazley

- BOXX Insurance

- Chubb

- Intact

- QBE

- Travelers Canada

- Trisura

- Wawanesa

- Zurich Canada

Insights

Methodology

To identify the best cyber insurers in Canada for 2026, Insurance Business Canada tapped into its extensive broker and reader community. The research team gathered insights through multiple survey channels across its nationwide audience, inviting brokers to vote on the cyber insurers they believe deliver the strongest value in today’s market.

Insurers that received notable broker support were invited to participate further in the process, including the opportunity to submit a detailed entry outlining the strengths of their cyber policies and products. These submissions provided insight into coverage features, product performance, claims support, underwriting expertise, and how their solutions help brokers and clients manage cyber risk.

Combining broker feedback with information provided through insurer participation, IBC evaluated each entry and identified the top performers. Winners were ultimately selected based primarily on overall broker support, with additional consideration given to demonstrated excellence in product quality, claims handling, underwriting expertise, and broker relationships.

© 2026 Insurance Business Canada. All rights reserved. This report is produced for informational purposes. For the most current policy details, coverage terms, and premium information, consult a licensed insurance broker.

Keep up with the latest news and events

Join our mailing list, it’s free!