Jump to winners | Jump to methodology

Canada’s best insurance claims carriers of 2026

This year’s best insurance claims carriers earn brokers’ trust when losses are at their highest, and demonstrate what makes a claims experience worthwhile

By Insurance Business ■ June 2026

Speed was once a differentiator.

Now it’s the floor.

In 2026, brokers, commercial clients, and policyholders expect more than fast. They expect consistency, transparency, and sound decision-making from first notice through resolution. The strongest claims operations cut uncertainty early, establish coverage positions sooner, and use technology to simplify handling, without sacrificing judgment or human support.

Those expectations are landing at a difficult moment. Catastrophe losses remain elevated. Cyber incidents keep evolving. Litigation is stretching longer in key areas. And clients now expect real-time visibility into where their claim stands.

The 5-Star Claims ranking, produced through broker nominations, insurer submissions, and Insurance Business Canada’s research, identifies the carriers delivering the strongest claims experience across communication, responsiveness, operational consistency, technology, and broker support. More than 200 broker evaluations and 18 insurer nominees shaped this year’s results, with final selections weighing both quantitative ratings and qualitative claims performance.

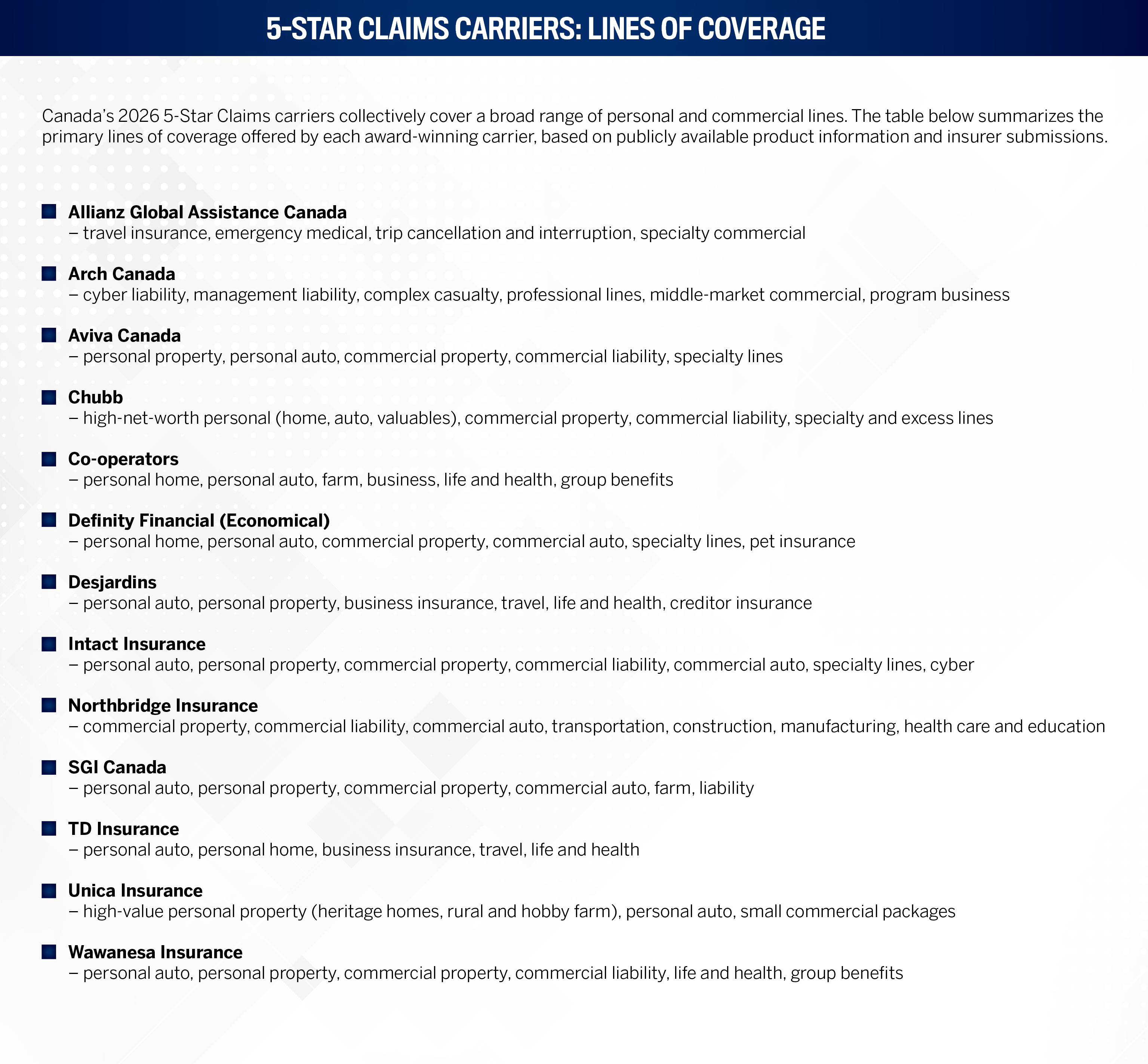

The top insurance claims carriers in Canada for 2026 are: Allianz Global Assistance Canada, Arch Canada, Aviva Canada, Chubb, Co-operators, Definity Financial (Economical), Desjardins, Intact Insurance, Northbridge Insurance, SGI Canada, TD Insurance, Unica Insurance, and Wawanesa Insurance. Each earned the 5-Star Claims designation through broker-validated performance across claims handling, responsiveness, operational consistency, technology, and broker support.

The scale of recent losses makes the stakes clear. In the summer of 2024 alone, the Insurance Bureau of Canada recorded approximately 250,000 claims and more than $8 billion in insured losses from four catastrophic events – a 443 percent increase over the 20-year average. The full-year 2024 total reached $9.1 billion in insured catastrophic losses, the highest annual total ever recorded in Canada, according to a CatIQ report published in January 2026. A year later, insurers had closed 92 percent of claims from the July 2024 Toronto and southern Ontario flooding, and 86 percent from the Calgary hailstorm.

Canada's insured catastrophe losses by year

2024 shattered all previous records — $9.1 billion in full-year insured catastrophic losses, revised upward from the initial $8.5B estimate as individual event figures were updated through 2025 (CatIQ, January 2026). Four events in 27 days accounted for more than $8 billion of that total.

Sources: CatIQ, January 2025 (initial estimate); CatIQ, January 2026 (revised full-year 2024 total of $9.1B); Insurance Bureau of Canada. Figures in CAD billions. The 2024 figure reflects CatIQ's most recent full-year total as of January 2026, revised upward from the initial $8.5B estimate as individual event loss figures were updated.

Complexity is rising across every line. CatIQ data shows insured catastrophic losses in Canada reached $2.4 billion in 2025, with societal losses at $3.4 billion. On the cyber side, ransomware, business email compromise, and funds transfer fraud continue to shift, making yesterday’s playbook insufficient.

The response across the market has been to go deeper on technology. Leading carriers are using AI, automation, analytics, and digital intake to cut delays, sharpen triage, strengthen fraud detection, and free experienced adjusters for the decisions that require their judgment.

Keegan Iles, national insurance leader and partner at PwC Canada, puts it plainly: “The challenge and opportunity for claims insurers today is to be digital first in service and delivery, while also retaining the human element where it counts most for customers. We’re at a tipping point where we can agentify many processes in ways that can reshape insurance claims management and support. But empathy, and how you support people during difficult times, will always be an essential feature of claims.”

The insurers recognized this year describe claims as an end-to-end service model, built on earlier claim direction, specialist expertise, disciplined workflows, broker communication, and embedded digital capability. What sets the strongest operations apart is their ability to combine speed with consistency, communication, and trust across the full life of the file.

Five questions to ask a carrier before a loss occurs

Choosing a claims carrier before a loss is the only time you have full negotiating leverage. These are the questions brokers and risk managers consistently wish they had asked earlier.

What are your documented service standards for first contact and adjuster assignment?

Verbal commitments don't tell you what happens when a CAT event hits and every adjuster is stretched. Ask for the written standard and ask how it held up in 2024 — Canada's costliest catastrophe year on record.

Do you have adjusters with specific expertise in the lines I'm placing?

Generalist handling on a complex cyber or commercial liability file carries real risk. Find out whether your file will be assigned to a specialist or whoever is available when the claim lands.

How do you handle coverage ambiguity?

The carriers that consistently earn the strongest broker ratings lean toward the insured's position when policy language is unclear. Ask directly what the carrier's philosophy is — and ask for a real example.

How will you keep me informed as my client's broker throughout the file?

Brokers who have to chase for updates are managing a client relationship breakdown that wasn't their fault. The best carriers treat broker communication as a structured responsibility, not an occasional courtesy.

How did your operation perform during the summer 2024 catastrophe events?

Canada's 2024 catastrophe season generated $9.1 billion in insured losses — the highest on record. How a carrier performed under that pressure, and what it structurally changed as a result, is more revealing than any service standard document.

Why claims handling in Canada is harder than ever

Claims departments aren’t just processing more files. They’re processing harder ones.

Economic pressure, climate losses, regulatory change, and rising customer expectations are all converging on claims operations at the same time, according to EY’s Canadian Insurance Outlook 2026 (March 2026). The demand cuts across every line. Property teams are absorbing weather-related loss volume and repair-cost inflation. Cyber teams are tracking ransomware, business email compromise, and funds transfer fraud. Liability files are more contested, with litigation funding and class-action activity reshaping settlement strategy.

The operational ask is clear: resolve routine claims faster, and direct experienced adjusters toward the files that actually need them.

Iles says digital access is now a baseline service expectation, but it can’t replace advice or human support.

“Being available digitally provides immense distribution and customer value, and portals form an integral part of that strategy,” he says. “Meeting your customers where they are, whether through digitally guided processes or on the phone getting advice from agents, these are all essential channel capabilities for a 21st-century insurer.”

Catastrophe losses have permanently raised the baseline

The summer of 2024 rewrote the record books. Four catastrophic events in 27 days – flooding, wildfires, and hailstorms – generated more than $8 billion in insured losses on their own. The full-year 2024 total reached $9.1 billion, the costliest year for insured catastrophic losses in Canadian history (CatIQ, January 2026). Flooding, wildfires, hailstorms, and severe weather hit in rapid succession, straining adjusters, restoration networks, and internal handling teams all at once.

Insurance Bureau of Canada’s In Brief report put a finer point on it. In just 27 days across July and August, four catastrophic events generated approximately 250,000 claims and more than $8 billion in insured losses – 50 percent more claims than Canadian insurers typically receive in an entire year.

Last year (2025) brought some relief, but not much. CatIQ recorded $2.4 billion in insured catastrophic losses, ranking the year second for total catastrophes declared and first for fire catastrophes. The volume has eased, the strain hasn’t.

Insurers are responding by rearchitecting for surge, not just recovery. Deloitte’s 2025 Insurance M&A and Technology Outlook notes carriers are deploying cloud infrastructure, AI-supported service delivery, geospatial triage, and virtual adjusting to scale faster when volume spikes. The operational decisions made now increasingly determine how quickly a customer’s file moves from first notice to resolution.

Summer 2024 — Canada’s four catastrophic events

In less than five weeks, four consecutive disasters produced Canada's costliest insurance season on record, generating over a quarter of a million claims.

July 15 — Toronto flooding | July 22 — Jasper wildfire | Aug 5 — Calgary hailstorm | Aug 9 — Hurricane Debby remnants

Sources: CatIQ one-year loss estimates (August 2025); Insurance Bureau of Canada In Brief report, "2024 Summer of Catastrophe across Canada" (October 2025).

Cyber and liability are the hardest files

in the book

Two lines are driving disproportionate complexity: cyber and liability.

Coalition’s 2026 Cyber Claims Report found initial ransomware demands jumped 47 percent year over year in 2025, even as many businesses held firm and invested in cyber resilience. Business email compromise and funds transfer fraud continued to generate significant losses.

Liability is grinding harder, too. Markel Canada president and managing director David Crozier remarked in February 2026 that files are taking longer to close and more claimants are willing to test litigation where they once would have settled.

“We are seeing an increase in the number of people testing litigation where they might have settled in the past,” he says.

The implication for insurers is straightforward. Technical expertise, early coverage analysis, and disciplined file management are competitive necessities.

Vinita Jajware-Beatty, president and board chair of the Toronto Insurance Women’s Association and corporate director for infrastructure, risk, and insurance, is direct about where the biggest efficiency gains come from: establishing a clear coverage position at the outset and holding to it. In her view, the carriers that reduce friction most effectively are those that commit early, communicate their reasoning clearly, and avoid relitigating decisions – building defined escalation pathways that reduce uncertainty across legal, operational, and governance layers.

She says, “Specialist expertise improves accuracy, speeds up resolution, and reduces unnecessary disputes. Without it, claims handling can become disconnected from the actual operational and financial realities of the loss.”

Cyber claims — ransomware demand and resistance trends

Ransomware actors are demanding more, but insured businesses are increasingly refusing to pay, pointing to improved resilience and carrier-supported incident response.

Sources: Coalition 2026 Cyber Claims Report (March 2026); Coalition 2025 Cyber Claims Report (May 2025). Canada-specific average loss data from Coalition / SC Media, May 2025.

How AI is changing insurance claims handling in Canada

Insurers aren’t experimenting with AI anymore. They’re running it.

KPMG’s 2025 Insurance CEO Outlook (January 2026) found 73 percent of insurance CEOs now rank AI as a top investment priority, with many allocating 10–20 percent of technology budgets to AI initiatives. According to the Insurance Trends Outlook 2026, AI is being integrated across underwriting, fraud detection, workflow management, customer service, and claims handling.

On the claims side specifically, carriers are using AI and analytics to automate intake and documentation review, flag potential fraud earlier, improve routing decisions, accelerate settlement evaluation, and generate faster customer updates, among other applications. The goal is freeing experienced adjusters to focus on the files that need them.

Jajware-Beatty frames the technology question clearly. “Technology is important, but it should enhance judgment, not replace it. Its value lies in real-time visibility, centralized communication, and better data capture for trend analysis,” she says.

That balance between automation handling the routine and humans owning the complex is what separates Canada’s strongest claims operations from the rest.

Insurance CEO AI investment priorities — KPMG 2025 survey

Based on 110 insurance CEOs globally (life, non-life, reinsurance, and broking). AI is reshaping claims, underwriting, and customer experience — and Canada's insurers are leading the sector's adoption curve.

Sources: KPMG 2025 Insurance CEO Outlook, KPMG International (January 2026) — 110 insurance CEOs surveyed. Canadian Chamber of Commerce Business Data Lab, Business Insights Quarterly Q4 2025. Insurance Business Canada (February 2026).

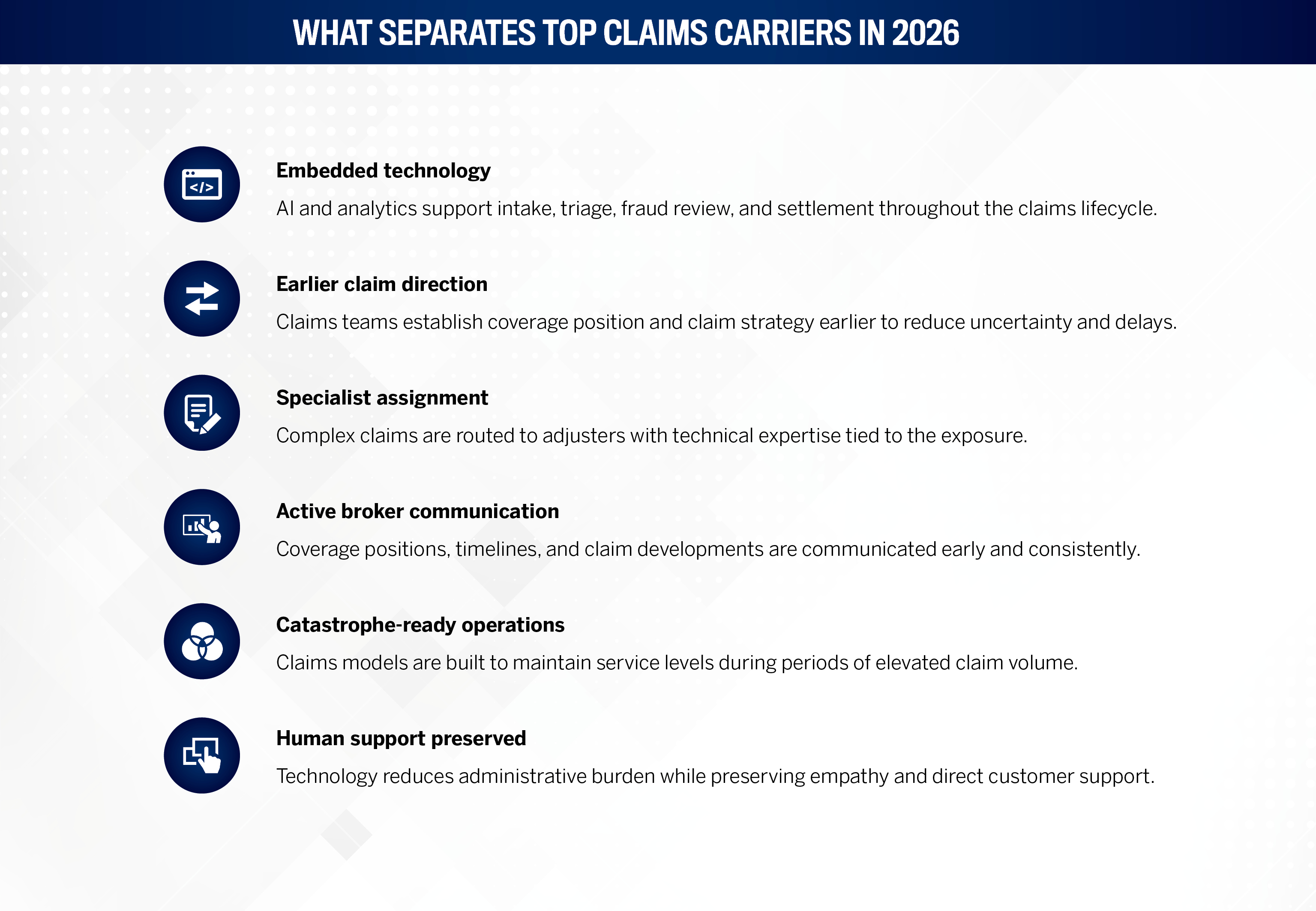

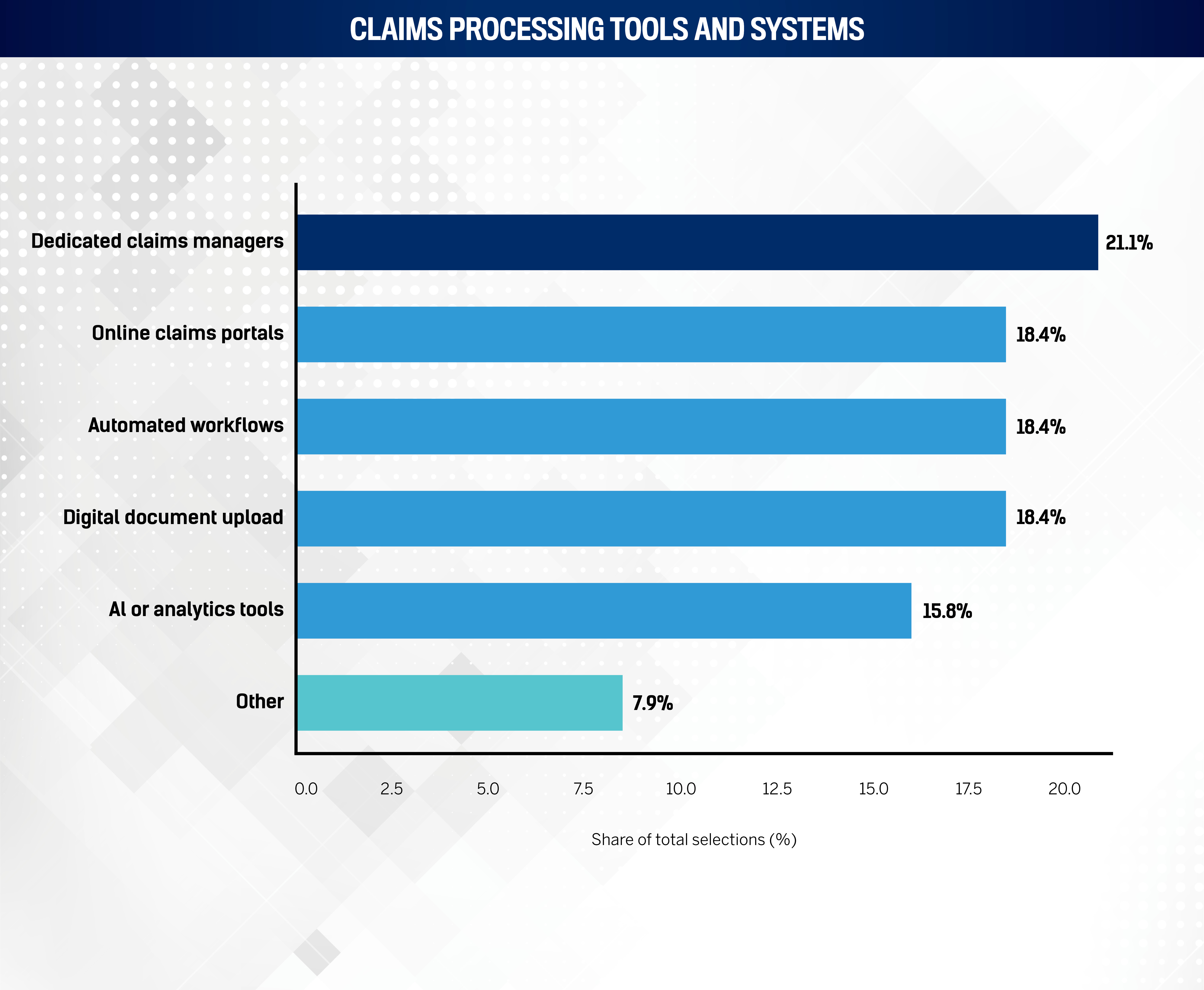

What defines a 5-Star claims carrier

Technology is in the workflow, not beside it

The strongest carriers aren’t piloting digital tools. They’ve built them into how claims actually run.

AI, automation, analytics, and digital intake are now embedded across triage, fraud review, assignment, communication, and settlement. The objective is fewer delays, better visibility, and more time for experienced adjusters to focus on judgment and customer support.

Deloitte Canada notes that leading insurers are designing always-on customer journeys where policyholders can initiate claims, upload documents, receive updates, and track status across multiple digital channels.

Dennis Schnadthorst, head of operations travel Americas at 5-Star winner Allianz Global Assistance Canada, says the real test of digital intake is whether it removes friction for the customer.

“We want to keep it as simple as possible and really focused for our customers so that we don’t ask for 50 different information and documents, but just focus on the most important ones,” he explains.

On end-to-end automation, he’s direct about the impact. “New technology can process claims payment end to end without a human touch, which of course significantly reduces the claims life cycle, and thus, the waiting time for customers.”

But Schnadthorst is clear that automation doesn’t replace human support when it matters.

“It allows our associates to have time when customers really need to talk to a human being. This is when they are really in a difficult situation like medical emergency when they are travelling,” he says.

Coverage positions are being set at

first notice, not later

The best claims operations don’t wait to form a view. They establish coverage direction early, communicate it clearly, and hold to it.

Prolonged timelines, inconsistent handling, and shifting positions are among the industry’s most persistent sources of friction. The carriers separating themselves are tackling that problem at intake.

Jajware-Beatty is direct about where the inefficiency lives. “Provide clear, consistent decisions early. The biggest inefficiencies come from shifting positions, unclear rationale, and re-litigation of issues,” she says.

5-Star honouree Northbridge makes coverage thinking a day-one discipline.

“Our team is educated, trained, and coached to think about coverage from the moment a claim is reported,” says Evan Di Bella, senior vice president of claims. “If we identify a potential coverage gap, we believe the insured should be informed as early as possible, often at the onsite inspection, so we can set clear expectations about what the remainder of the investigation will look like and how decisions will be made.”

Brokers are also brought in at intake, not after the fact.

“This ensures there are no surprises and gives brokers the opportunity to raise concerns, advocate for our mutual clients, and help manage expectations.”

Allianz extends that transparency to the point of sale. Schnadthorst says the goal is to eliminate surprises before the claim ever happens.

“We start by helping customers understand upfront, already when they buy a policy, what is covered and what isn’t. Our goal is really to avoid surprises later on,” he says. “We explain the decision clearly and [make it] really transparent to our customers.”

Specialists handle the files that need them

Cyber, infrastructure, liability, catastrophe, and complex commercial files don’t respond to generalist handling. The carriers succeeding in these lines are building teams around specialist capability.

Iles says expanding into new product areas has made this a necessity, not a differentiator.

“Claims is a core insurance discipline, and it’s becoming increasingly complex to meet the growing market focus on expanding product lines to cover more types of risk,” he says. “To meet that complexity, insurers need to proactively identify the right capabilities and talent to manage new risks and complex claims.”

This year’s 5-Star winners describe assignment models built around expertise and deliberate file segmentation.

At Northbridge, complex or high-severity claims are assigned to senior adjusters who have deep experience and specialized training. Those files are intentionally balanced with appropriate caseloads for file complexity, recognizing that complex claims require more time, judgment, and focus,” Di Bella explains.

Allianz runs dedicated streams for routine and complex files, keeping each moving at the right pace.

“We deliberately separate our model. We have one team focused on core benefits, and another team focusing on complex claims,” says Schnadthorst. “It keeps the overall operation more nimble, ensuring that more demanding files are handled with the right focus without slowing down the service for the much broader portfolio.”

Trust is built file by file

Across this year’s winners, one theme came up more than any other: consistency.

The strongest claims operations treat every touchpoint as part of a trust relationship. Regular updates, plain-language explanations, proactive broker communication, active ownership from intake through settlement. Not because it’s policy, but because it’s what clients remember.

Jajware-Beatty puts it plainly. “Claims is the moment of truth in the insurance value chain. It defines trust, outcomes, and long-term relationships.”

Northbridge structures its review process to reinforce that standard. Coverage gaps go through multiple layers of management before a decision is communicated.

Di Bella says, “Any significant gap is reviewed through multiple layers of management to ensure consistency, fairness, and appropriate treatment of the customer.”

And when the policy language leaves room for interpretation, the carrier’s default is clear.

“Where there is ambiguity, we intentionally lean toward the insured’s position,” Di Bella explains.

What separates the strongest claims operations is the ability to deliver technical expertise, consistent communication, and genuine customer support on every file.

5-Star Claims carrier: Northbridge Insurance

For Northbridge Insurance, claims handling starts before the adjuster picks up the phone. Coverage review begins at first notice of loss, technology captures intake in real time, and the insured is kept informed at every step. That operating discipline, applied consistently across more than 300 claims professionals nationwide, is what earned Northbridge a place among this year’s 5-Star winners.

Northbridge Insurance — claims service performance

Northbridge's commercial P&C claims model is built around speed, specialist assignment, and field-level resolution capability — with measurable service standards across its national network.

Source: Northbridge Insurance insurer submission, IBC 5-Star Claims 2026 research process. Industry contact benchmark from BrokerLink / Reuters (December 2025).

The numbers behind that model are notable. Northbridge’s claims call centre answers within 20 seconds more than 91 percent of the time. In 92 percent of cases, an adjuster contacts the customer within three business hours of the claim being reported. Field adjusters frequently issue payment drafts on the first site visit. These aren’t aspirational targets. They’re the baseline the carrier holds itself to.

-

91 percent: calls answered within 20 seconds

-

92 percent: adjuster contact within 3 business hours

-

300+: claims professionals deployed nationally

Technology sits at the centre of that speed. At intake, AI-driven tools enable real-time claim creation and information capture, cutting administrative load so adjusters can immediately focus on the insured. Throughout investigation, digital tools assist with scoping and evaluating damage, helping adjusters prepare accurate settlement offers more efficiently. After closure, customer feedback feeds directly into a continuous improvement process the carrier calls Listening for Excellence, identifying friction points and removing unnecessary complexity from the experience.

Di Bella explains the long-term ambition is to close the gap between loss and resolution entirely.

“We are on a continuous improvement journey, with the long-term goal of evaluating and settling claims as close to real time as possible. By shrinking the overall length of the claims process, we help insureds return to their homes, businesses, or normal lives more quickly.”

On complex and high-severity files, Northbridge uses a committee review model to bring multiple experienced perspectives to the most difficult decisions. Senior adjusters handling those files have appropriate caseloads for file complexity, allowing the time and focus those claims demand. For catastrophe response, mobile technology allows CAT adjusters to complete onsite assessments and initiate settlement processing in the field, without waiting to return to office systems.

Northbridge’s sector depth adds another layer of capability. The carrier serves clients across health, education, construction, manufacturing, and transportation, and invests in hundreds of annual technical training hours through its Northbridge University Faculty of Claims to keep adjusters current on sector-specific complexities. That expertise extends to cross-border claims capabilities for transportation clients, where regulatory and jurisdictional factors can complicate resolution significantly.

The through-line across all of it, Di Bella says, is ownership. Northbridge takes full responsibility for driving the file forward, so neither the broker nor the insured has to chase for updates or manage the process themselves.

“Our goal is to respond to losses wherever the policy allows. Where there is ambiguity, we intentionally lean toward the insured’s position,” he says.

5-Star Claims carrier: Allianz Global Assistance Canada

Travel insurance claims are different from almost any other line. The customer is usually far from home, under stress, and needs an answer quickly. Allianz Global Assistance Canada has built its claims model around that reality, with decades of experience supporting Canadian travellers and a 4.6 out of 5 customer satisfaction score according to internal customer data provided in its insurer submission.

The carrier operates as a true end-to-end provider, with in-house teams spanning emergency travel assistance, medical professionals including physicians and nurses, claims adjudicators, and fraud experts. That single-source structure is deliberate. Rather than managing hand-offs between third parties, Allianz controls the full customer journey, which gives broker partners clearer accountability and consistent quality across every stage of a claim.

-

4.6/5: customer satisfaction score (internal customer data, Allianz submission)

-

35+: years supporting Canadian travellers

-

90+: countries with virtual care access

The claims portal sits at the centre of the intake experience. Customers can file digitally from a mobile-optimized interface, upload documents, identify anything missing before submitting, save and return to incomplete submissions, and track status in real time. A phone-to-portal transfer option also lets customers who call in move seamlessly to digital if they prefer to continue online. The result is fewer follow-ups and shorter cycle times.

Schnadthorst says the real measure of technology is whether it removes burden from the customer rather than creating it.

“Technology materially changes claims handling when it is able to remove frictions for the customers. The result is a process that is much faster, easier, and also more accurate for customers," he explains.

On complex claims, Allianz takes a proactive adjudication approach. Rather than waiting for customers to gather documentation, examiners contact medical providers and service partners directly on the customer’s behalf. When information is still missing during a review, examiners reach out personally rather than sending generic email requests.

That hands-on approach is especially important for travel medical claims, where customers may be navigating unfamiliar health systems abroad. Allianz has expanded virtual care services to more than 90 countries, including a self-service option that connects customers directly with physicians overseas, reducing the need to visit a hospital or pay out of pocket and then file.

Payment speed is also a priority. Approved claims are paid primarily through electronic funds transfer, typically within one to two business days, with a clear explanation of benefits accompanying each payment.

Schnadthorst says getting customers back to normal as quickly as possible is the underlying objective across all of it.

“We want to provide peace of mind to our customers from the moment they buy a policy with us. Our customers should be aware and sure that when they travel, we take care of them when they are in a not-so-good situation.”

Allianz is investing further in claims automation and fraud detection, and plans to launch a new app in 2026 that consolidates policy management, global doctor access, and claims submission in a single interface, with direct SMS communication built in.

What’s changing in claims operations

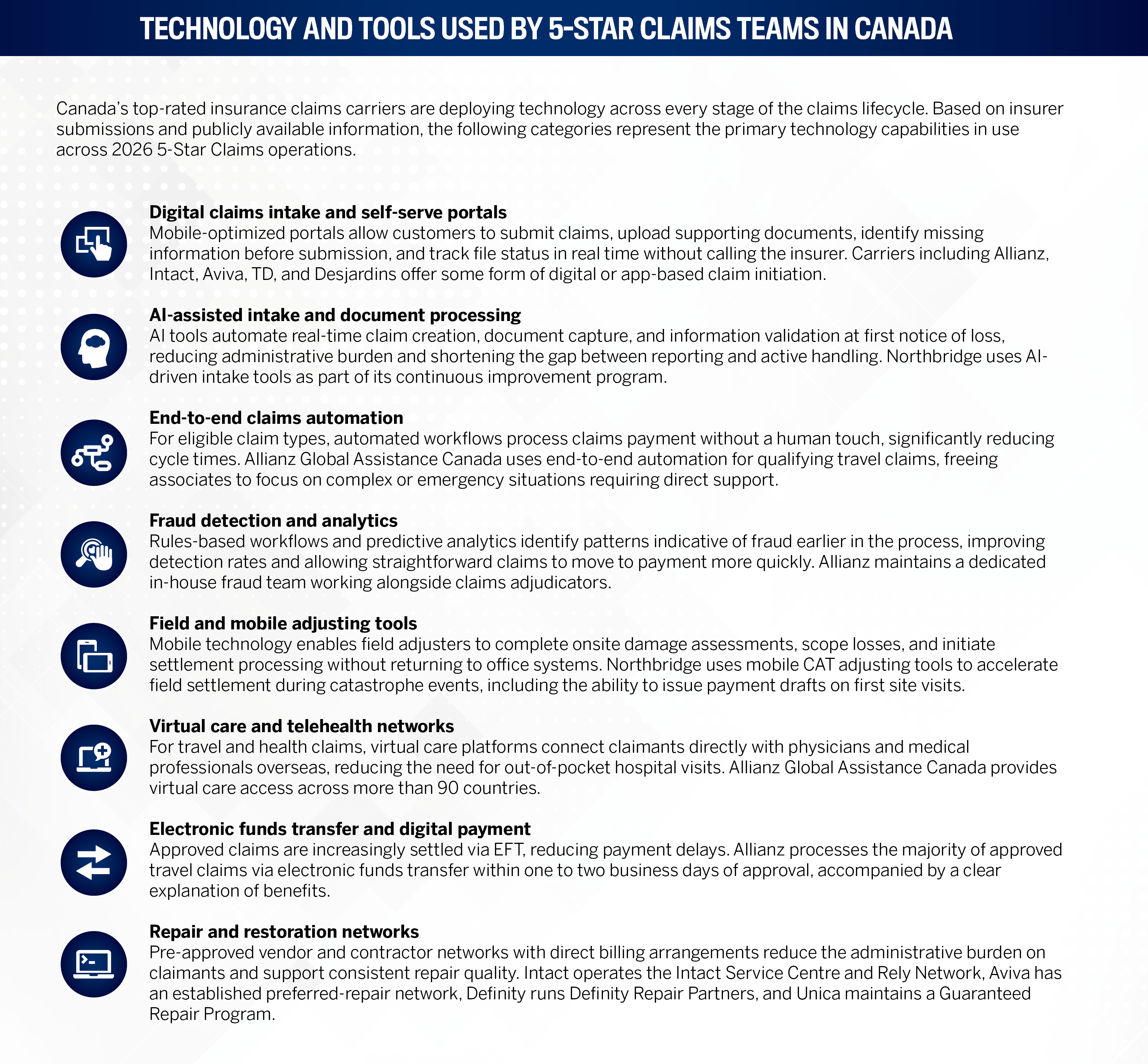

Canada’s 5-Star claims carriers describe innovation not as a single transformation, but as a steady accumulation of targeted improvements across technology, service, and governance. Six themes emerged consistently across submissions – and in each case, carriers could point to specific changes already in operation, not in planning.

Digital access

Expanded portals and mobile tools now let customers submit claims, upload documents, and track status in real time, reducing follow-ups and improving visibility throughout the process. Allianz Global Assistance Canada’s mobile-optimized portal lets customers save incomplete submissions, identify missing documents before filing, and transfer seamlessly from phone to digital. Intact’s app enables end-to-end auto claim initiation, towing arrangement, and real-time tracking without a single call.

Automation

AI-supported tools are reducing manual administrative work, freeing experienced adjusters to focus on decisions, analysis, and customer support. Northbridge uses AI-driven intake to enable real-time claim creation and information capture at first notice, cutting the gap between reporting and active handling. Allianz processes qualifying travel claims end-to-end without human intervention, a model that measurably shortens cycle times and directs associate attention to complex or distressed files.

Speed

Operational changes are shortening end-to-end timelines, accelerating complaint resolution, and improving access to payments, repairs, and services. Intact’s 30 Minute Claims Guarantee commits to starting a claim within 30 minutes of answering the call or paying compensation. Allianz settles the majority of approved claims via electronic funds transfer within one to two business days. Northbridge field adjusters frequently issue payment drafts on the first site visit.

Customer experience

Clearer communication, redesigned claims instructions, and more personalized guidance are improving how customers experience the process from start to finish. Several carriers cited behavioural economics as an input into how claims correspondence is written – restructuring instructions to reduce confusion at high-stress moments. Northbridge’s Listening for Excellence program feeds customer feedback directly into continuous improvement, identifying friction points after each file closes.

Service networks

Broader vendor networks, virtual care services, and global provider relationships are expanding access, enabling direct billing, and improving the quality and speed of support. Allianz Global Assistance Canada provides virtual care access across more than 90 countries, connecting travellers directly with physicians overseas and reducing out-of-pocket hospital costs. Intact’s Rely Network and Definity’s Repair Partners bring pre-approved contractors and direct billing into property and auto claims, removing a significant administrative burden from clients managing repairs.

Governance

Updated internal policies, service standards, and oversight frameworks are reinforcing consistency, improving reporting quality, and aligning operations with client and regulatory expectations. Northbridge routes all significant coverage gaps through multiple layers of management review before a decision is communicated – a governance model designed to ensure consistency, fairness, and appropriate treatment at every file. Aviva’s Claims Service Satisfaction Guarantee formalizes accountability for the claims experience at the carrier level.

How 5-Star carriers approach claims

The 5-Star standard

Across submissions and interviews, Canada’s top-rated claims carriers describe a consistent operating philosophy. Nine principles define how the strongest operations run.

1 Customer first

Every claim is treated as unique. Responsiveness, transparency, and genuine care guide each interaction, not just process compliance.

2 Proactive communication

Teams provide regular updates, explain next steps, and help customers understand where their file stands at every stage.

3 Early engagement

Files are reviewed, assigned, and actively managed from first notice. Early contact and rapid initial assessment set the direction for the whole file.

4 Specialist expertise

Claims are handled by professionals with deep knowledge of specific lines, supporting better decisions on files with genuine complexity.

5 Technology that works

Digital tools, analytics, and AI support intake, triage, fraud detection, and workflow management. The goal is better decisions, not just faster ones.

6 Consistent process, flexible handling

Defined workflows and governance provide a reliable baseline. Handling is adapted to the nature and exposure of each file.

7 Fair and efficient outcomes

Straightforward claims move through streamlined processes. Complex ones get deeper review. Both are resolved with the same focus on fairness and timeliness.

8 Broker transparency

Brokers are kept informed on coverage, timelines, and file strategy, so they can support clients and manage expectations throughout the process.

9 Claims as a trust moment

The claim is where insurers deliver on their promise. The strongest carriers treat every file as a chance to reinforce, not just fulfill, that commitment.

Industry expert Q&A section

What the experts want from claims in 2026

The claims conversation in Canada right now comes down to one tension: How far can carriers push technology before they lose the human element that actually builds trust? Two industry leaders – one advising carriers on transformation, one sitting on the other side of the table as a client and governance expert – give their unfiltered view of what the market is getting right, where it’s still falling short, and what they expect from Canada’s claims carriers in 2026.

Keegan Iles

National Insurance Leader and Partner, PwC Canada

What do you want from a claims insurer

in 2026?

The best insurers will pair the efficiencies and speed of AI with human care where it matters, so the customer experience is both efficient and thoughtful. Getting that balance right is the defining challenge of the moment.

How do you see specialist expertise fitting into a claims operation that is also investing heavily in technology?

They aren’t in tension. Matching the growth of the business to the claims skills it will require is an ongoing juggling act. As insurers expand into new product lines and more complex risk categories, the capability required to manage those claims has to keep pace. Technology can support that work, but it can’t substitute for the judgment that comes with deep technical experience.

Matching how the business is growing to what kinds of claims should be expected, and ultimately what claims management skills will be required, continues to be a juggling act.

Where does technology create the most value inside a claims operation?

The real opportunity is scalability. Enabling customers to access information on their own terms, whether it’s a billing question, a product feature, or the status of a claim, becomes increasingly important as AI takes on more of the delivery. Having that information accessible and scalable isn’t just a convenience. It’s how insurers stay relevant at the moments that matter most.

Enabling ‘as you need’ input on product features, whether your bill is coming due, or the status of your claim, are all critical information moments for carriers to deliver on.

Vinita Jajware-Beatty

President and Board Chair, Toronto Insurance Women’s Association; Corporate Director, Infrastructure,

Risk and Insurance

What do you want from a claims insurer

in 2026?

A true risk partner, not just a payer of claims. That means alignment between what was underwritten and how claims are actually handled, transparency in decision-making, and proactive communication throughout. The gap between underwriting intent and claims execution is where trust erodes fastest.

What is the most common problem you encounter when dealing with a

claims insurer?

Misalignment between underwriting intent and claims handling. It tends to show up as narrow interpretations of coverage or overly defensive positions on files. From a governance perspective, that kind of uncertainty in the total cost of risk is more damaging than the outcome of any single claim.

Where does technology create the most value in claims, beyond tracking and

status updates?

The real opportunity is upstream. Claims data should be feeding back into underwriting and risk prevention, not just recording what happened. That closed loop between claims experience and risk strategy is where technology can genuinely shift outcomes, rather than simply improve how quickly information is displayed.

The real opportunity is using claims data to inform underwriting and risk prevention, not just to track claim status.

Which insurance claims carrier is best for commercial lines in Canada?

The best insurance claims carrier for commercial lines in Canada depends on the specific lines of business, risk profile, and geography of your clients. Several 2026 5-Star Claims carriers have distinct strengths in commercial: Northbridge Insurance leads for mid-market commercial P&C across construction, transportation, manufacturing, and health care; Arch Canada specializes in complex casualty, cyber liability, and management liability; Chubb covers high-value commercial and specialty risks; and Intact Insurance offers the broadest national commercial capacity with large-scale catastrophe-handling infrastructure.

For brokers placing cyber or management liability, Arch Canada’s specialist teams and local binding authority make it a strong choice for complex commercial risks. For property-exposed commercial clients in Western Canada, SGI Canada’s regional expertise and broker-channel model bring deep familiarity with Alberta and Saskatchewan exposures including hail, flood, and wildfire. For travel-dependent commercial operations, Allianz Global Assistance Canada’s end-to-end emergency assistance and claims model provides coverage and support across more than 90 countries. The 5-Star Claims research process captures broker experience by carrier and line of business, making it one of the most reliable tools available for matching commercial risk to the right claims carrier in Canada.

Understanding uncertainty

Thirteen carriers. Over 200 broker evaluations. One consistent finding across all of them. The data from this year’s research points in one direction. Catastrophe losses are structurally elevated. Cyber files are getting more technically demanding. Litigation is adding friction to liability claims that once settled cleanly. And clients, whether a small business owner filing a property claim or a risk manager overseeing a complex infrastructure portfolio, are measuring their insurer against a service standard that keeps rising.

The carriers recognized this year saw those pressures coming and stopped treating them as exceptions.

The strongest operations have rebuilt around a simple insight: uncertainty is the real cost of a poorly handled claim. The weeks of unclear communication, shifting positions, and unresolved questions erode trust long before a file closes. The carriers earning the highest broker ratings are the ones that made uncertainty reduction a design principle.

Technology is accelerating that shift, though it isn’t the source of it. The carriers using AI most effectively were already disciplined about early coverage direction, specialist assignment, and broker communication. Automation made those disciplines faster and more consistent.

What the experts in this report keep returning to is also the hardest thing to systematize: the moment when a client needs a human being on the other end of the line, and gets one.

In a market growing more complex by the year, that standard – a human being on the other end of the line when it matters most – is what separates the carriers clients return to from the ones they leave after a claim.

Frequently asked questions about

claims carriers in Canada

Which insurance claims carriers in Canada have the best service, and how are they ranked?

The top insurance claims carriers in Canada for 2026, as ranked by Insurance Business Canada’s 5-Star Claims research, are: Allianz Global Assistance Canada, Arch Canada, Aviva Canada, Chubb, Co-operators, Definity Financial (Economical), Desjardins, Intact Insurance, Northbridge Insurance, SGI Canada, TD Insurance, Unica Insurance, and Wawanesa Insurance. Rankings are determined through broker nominations and insurer submissions, with final scores based primarily on broker ratings across claims handling, responsiveness, communication, technology, and service consistency. The full methodology is below.

The top insurance claims carriers in Canada for 2026 are identified through a comprehensive research process run by Insurance Business Canada, drawing on its national network of brokers and industry professionals.

The process begins with broker nominations. Insurers that receive a sufficient volume of nominations are then invited to complete a detailed submission covering service standards, claims turnaround times, dispute resolution processes, technological capability, and broker support frameworks.

Final scores are based primarily on broker ratings across key performance indicators, with additional weight given to consistency of service and demonstrated claims outcomes. Both quantitative survey results and qualitative information from insurer submissions inform the final assessment.

The 5-Star designation is awarded to Canada’s best claims carriers – those that achieve outstanding broker ratings while demonstrating strong performance across claims management, operational efficiency, and broker engagement. It reflects how a carrier performs in practice, as experienced by the brokers who work with them every day.

What makes a top-rated insurance claims carrier in Canada stand out from the rest?

Top claims carriers are distinguished not by any single capability but by how consistently they deliver across several dimensions at once. Based on broker evaluations and insurer submissions, the strongest operations share a common set of characteristics.

They establish coverage direction early and hold to it. Shifting positions mid-file is one of the most common sources of friction in claims handling. The best carriers form a view quickly, communicate it clearly, and don’t relitigate decisions without cause.

They match the right expertise to the right file. Complex commercial, cyber, infrastructure, and catastrophe claims require specialist knowledge. Top carriers build their assignment models around that reality, with deliberate file segmentation and caseload management that protects the time and focus complex files demand.

They use technology to improve the experience, going well beyond internal workflow gains. The carriers earning the strongest broker ratings aren’t simply automating processes. They are using digital tools to reduce delays, improve communication, and give clients real-time visibility into where their claim stands.

They treat broker communication as a core responsibility, not an afterthought. Brokers are kept informed on coverage positions, timelines, and file developments so they can support clients throughout the process without having to chase for updates.

And they take ownership. The file moves because the carrier drives it forward, not because the client or broker follows up.

Why does claims handling matter so much when choosing an insurance carrier

in Canada?

Insurance is a promise. Claims handling is where that promise is either kept or broken. For most clients, the claims experience is the only direct test of whether their insurer actually performs as expected. Everything else, the policy wording, the premium, the coverage conversation at renewal, leads to this moment.

How a carrier handles a claim shapes the client relationship in ways that nothing else can. A claim that is managed with transparency, consistency, and genuine support builds trust that lasts well beyond the file closure. A claim that is handled poorly, with unclear communication, shifting coverage positions, or slow response, creates doubt that is difficult to recover from regardless of the outcome.

That dynamic is especially pronounced in commercial lines, where brokers are accountable to clients for the carriers they recommend. A poor claims experience reflects not only on the insurer but on the broker relationship. Conversely, a carrier that performs well at claims becomes one that brokers actively advocate for.

In a market where coverage terms and pricing across carriers are increasingly comparable, claims handling has become one of the clearest and most durable sources of differentiation.

What should Canadian brokers look for when evaluating and choosing a claims carrier?

When choosing an insurance claims carrier in Canada, brokers should evaluate documented service standards, specialist adjuster capability, coverage philosophy, broker communication practices, digital visibility, and catastrophe readiness. Carriers that score highest across all six areas – rather than excelling in one – consistently deliver the strongest claims experience. The key questions to ask before a loss occurs are below.

Choosing a claims carrier on price or brand alone leaves significant risk on the table. The questions worth asking before a loss occurs are the ones that reveal how a carrier actually performs when it matters.

Key areas to evaluate:

Response standards. How quickly does the carrier acknowledge a new claim, and how soon does an adjuster make contact? Service standards should be documented, not just described.

Specialist capability. Does the carrier have adjusters with genuine expertise in the lines most relevant to your clients? Generalist handling on complex commercial, cyber, or infrastructure files carries real risk.

Coverage philosophy. How does the carrier approach ambiguity in a policy? Carriers that lean toward the insured’s position and communicate their reasoning clearly are meaningfully different from those that default to a narrow reading.

Broker communication. Are brokers treated as partners throughout the file, or notified only when a decision has been made? Proactive, consistent communication with the broker is a reliable indicator of how the carrier will treat the client.

Technology and visibility. Can clients and brokers access real-time status on active files? Digital capability matters not just for efficiency but for the confidence it gives clients that their claim is being actively managed.

Catastrophe readiness. For property-exposed clients especially, how the carrier scales during high-volume events is as important as how it performs in normal conditions.

Broker networks, industry rankings, and peer referrals are all useful inputs. The 5-Star Claims process is specifically designed to surface this kind of operational performance data based on broker experience across a large volume of real claims.

How is AI actually changing insurance claims handling in Canada in 2026?

AI and automation are generating real operational change in Canadian claims, but the impact varies significantly depending on how a carrier has integrated the technology and what problem it was designed to solve.

The most tangible improvements are appearing in three areas. First, intake and documentation. AI-driven tools are enabling real-time claim creation, document capture, and information validation at first notice of loss. This reduces the administrative burden on adjusters and shortens the gap between when a loss is reported and when active handling begins.

Second, fraud detection and triage. Carriers are using analytics and rules-based workflows to identify patterns that warrant closer review earlier in the process, improving both detection rates and the speed at which straightforward claims can be cleared for payment.

Third, communication and status visibility. Digital portals and automated updates are giving clients and brokers real-time access to claim status, reducing follow-up calls and improving confidence that files are being actively managed.

Where technology is not yet replacing human judgment is on files that involve genuine complexity, coverage ambiguity, negotiation, or significant customer distress. The carriers performing best are using automation to protect the time and attention of experienced adjusters.

The broader opportunity, which leading carriers are beginning to act on, is using claims data to feed back into underwriting and risk prevention. That closed loop between claims experience and risk strategy is where AI may ultimately create its greatest value for both insurers and their clients.

How do Canada’s best insurance claims carriers perform during catastrophe events?

Catastrophe performance is one of the most meaningful tests of a claims carrier in Canada. The full year 2024 produced the costliest catastrophe period in Canadian insurance history, with $9.1 billion in insured losses from flooding, wildfires, hailstorms, and severe weather across the country (CatIQ, January 2026). Four of those events occurred in just 27 days, generating more than $8 billion in losses from the summer alone. How carriers performed during that period – and how quickly they closed files – is one of the most telling indicators of claims quality. The Insurance Bureau of Canada reported that by 2025, insurers had closed 92 percent of claims from the July 2024 Toronto and southern Ontario flooding, and 86 percent from the Calgary hailstorm.

Canada’s top-rated claims carriers are building operations specifically designed to scale during surge events, not just recover after them. Key indicators to look for include dedicated catastrophe response teams, mobile adjusting capability that enables field settlement without returning to office systems, and pre-built vendor and restoration networks with enough capacity to absorb high claim volumes without significant delays.For brokers placing property-exposed commercial or personal lines clients, asking how a carrier has performed during the last major catastrophe – and what structural changes they made as a result – is one of the most useful questions before a loss ever occurs. The 5-Star Claims research process specifically captures broker experience during peak-volume events, making it one of the most relevant data points for evaluating catastrophe readiness across the best insurance claims carriers in Canada.

Top Insurance Claims Carriers in Canada |

5-Star Claims

- Aviva Canada

- Chubb

- Co-Operators

- Definity Financial (Economical)

- Desjardins

- Intact Insurance

- SGI Canada

- TD Insurance

- Unica Insurance

- Wawanesa Insurance

Insights

-

Keegan Iles

Keegan Iles

National Insurance Leader and Partner

PwC Canada -

Methodology

How the best insurance claims carriers in Canada were selected

To determine the 5-Star Claims insurers for 2026, Insurance Business Canada conducted a comprehensive research process leveraging its national network of brokers and industry professionals. Brokers were invited to nominate insurers based on their experience with claims handling and overall service delivery.

Insurers that received a sufficient volume of broker nominations were invited to participate further in the process, including the opportunity to complete a detailed submission. These submissions outlined claims capabilities such as service standards, claims turnaround times, dispute resolution processes, technological innovation, and broker support frameworks.

The research team analyzed both the quantitative survey results and any qualitative information provided through insurer participation. Final scores were determined primarily based on broker ratings across key performance indicators, with additional consideration given to consistency of service and demonstrated claims outcomes.

The 5-Star Claims designation was awarded to those organizations that achieved outstanding broker ratings while demonstrating strong performance in claims management, operational efficiency, and broker engagement.

Keep up with the latest news and events

Join our mailing list, it’s free!