Annual inflation rate has been easing down after hitting a four-decade high in June 2022, according to the latest data from Statistics Canada (StatCan). Households across the country, however, continue to bear the brunt of the impact of the rising cost of living.

But what does this mean for insurance buyers?

In this part of our client education series, Insurance Business crunches the numbers to find out how inflation affects insurance rates in areas with the highest cost of living in Canada. We will also provide practical tips on how you can curb insurance expenses.

If you’re a consumer trying to work out an insurance budget, this guide can help you map out a feasible financial plan. Insurance professionals can also share this piece with their clients to educate them on the effects of high living costs on their premiums.

British Columbia has the highest cost of living among all provinces, according to a new report by Westland Insurance. Ontario ranked second, followed closely by Alberta.

At the other end of the spectrum is Newfoundland and Labrador, which is hands down the most inexpensive place for Canadians to live. Prince Edward Island and Québec joins the northeastern province on the list of provinces with the lowest cost of living.

To come up with the list, the Surrey-based P&C insurer compiled data from StatCan and the trade body Canadian Real Estate Association (CREA) and compared the numbers. Among the variables the study considered were income, food prices, rent, property prices, and transportation costs. The scores were then indexed and weighed to come up with a total rating of 100. Here’s the final ranking:

|

Rank |

Province |

Total score |

|

1 |

British Columbia |

79 |

|

2 |

Ontario |

71 |

|

3 |

Alberta |

67 |

|

4 |

Manitoba |

61 |

|

5 |

Saskatchewan |

60 |

|

6 |

Nova Scotia |

56 |

|

7 |

New Brunswick |

55.4 |

|

8 |

Quebec |

55.2 |

|

9 |

Prince Edward Island |

51 |

|

10 |

Newfoundland and Labrador |

20 |

Source: Westland Insurance

“British Columbia ranked among the top three most expensive provinces in every category, except accommodation, bills, and utilities expenses, where it placed fourth,” a spokesperson for Westland Insurance explains. “It's clear that the two most expensive provinces have exceptionally high house prices, but general living costs tend to be higher, too.”

The company’s data shows that British Columbia is among the costliest provinces for buying and renting property, purchasing a plane ticket, taking public transport, and accessing dental services and health care.

Property prices are also the highest, with the median home value at $996,460, more than twice the national average of $490,520.

Average house prices in Ontario rank next at $931,870. The province is also the most expensive place to buy fruit, vegetables, and furniture, and do home repairs.

“Newfoundland and Labrador's data paints the exact opposite picture,” the spokesperson notes. “Of the seven categories analyzed, Newfoundland and Labrador's expenses ranked among the cheapest three, except for accommodation, bills, and utilities.”

According to the study, Newfoundland and Labrador is the cheapest province for childcare, raising pets, rent, eye care, dental services, buying cars, and dining out. Its index score of 20 is 31 points lower than previous-placer Prince Edward Island.

“With remote working becoming increasingly popular, enabling more job opportunities outside of metropolitan areas, this province may be the easiest way to get on the property ladder and enjoy comparatively lower living costs while saving to buy,” the spokesperson adds.

One of the biggest factors that contribute to rising living costs is inflation. The Canadian government monitors inflation through a monthly consumer price index (CPI) that records pricing changes from a fixed “basket” of goods and services. This basket is separated into several categories, including food, shelter, clothing, transportation, and recreation. Each group is weighed accordingly to determine the country’s overall inflation rate.

To find out how inflation impacts insurance rates, Insurance Business will look at two categories within the CPI:

This index shows price changes of several property-related expenses, including homeowners’ and mortgage insurance.

This index tracks motor vehicle-related costs, including car insurance.

We will also compare data from the latest price index, which you can filter by province, along with available information from StatCan.

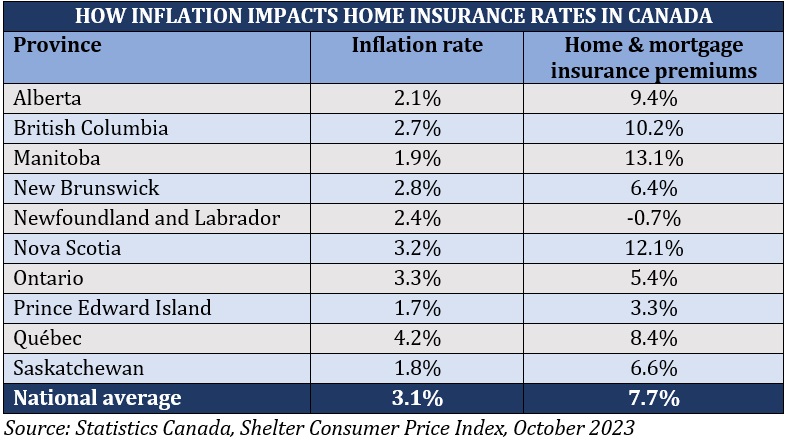

The latest shelter CPI has revealed that home and mortgage default insurance rates across Canada shot up 7.7%. Other shelter-related expenses that have a direct impact on premiums also increased. These include property and maintenance costs, which rose 3.5%.

Rental accommodation also went up 8.1%. This is typically covered by your home insurance policy if your property becomes uninhabitable due to an insured peril. Home replacement costs, another standard inclusion, decreased by a marginal 1.2%.

But while insurance companies are often responsible for shouldering these expenses, surging claims costs can likewise push up your home insurance premiums in the long run.

Here’s how inflation affects homeowner’s and mortgage insurance rates in different provinces, according to the price index.

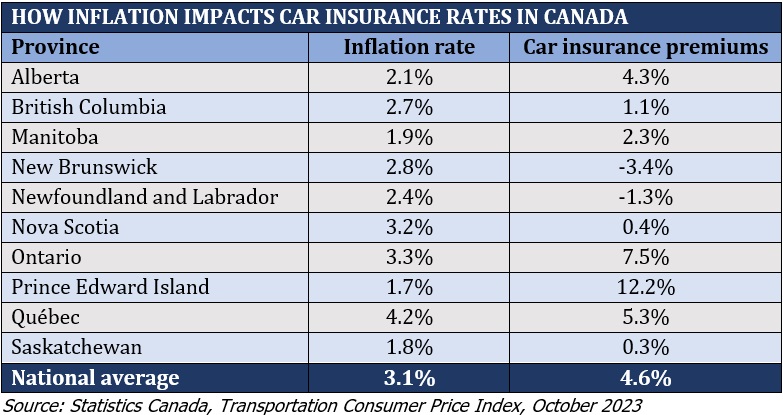

Car insurance premiums went up 4.6% across Canada because of inflation based on the latest price index.

Auto insurers use different metrics to determine insurance rates. These include the driver’s profile (age, gender, and driving history) and industry costs. A rise in the prices of vehicles and their parts can likewise increase the cost of a car insurance claim. Just like in other types of coverage, the more expensive the claim, the higher the premiums.

In the latest transportation CPI, vehicle parts, maintenance, and repair costs rose 5.6%. Vehicle prices also went up 1.5%. Meanwhile, rental vehicles, which your car insurance policy covers if your car is being repaired, decreased 2.2%.

Here’s a province-by-province comparison of the effect of inflation on car insurance premiums.

More Canadian households are experiencing financial uncertainty as inflation eats into their savings, a recent survey by Royal Bank of Canada (RBC) reveals.

The banking giant polled 1,508 adults and found that the high cost of living has topped Canadians’ list of worries. More than three-fourths of the respondents admit that they can’t save as much as they would like to because of rising living expenses. Of these, around half say they’ve never been more stressed about money.

The survey results also show that more than a third of those interviewed don’t have an emergency fund, weakening their financial flexibility further.

The majority of respondents are also worried about a potential recession. They’re concerned that it will be more difficult to weather an economic downturn today than in 2008.

Almost three quarters of the survey participants are anxious about taking in more debt if inflationary pressures continue into the next year. Of these, around a fifth say they may have to come out of retirement if that happens.

Home insurance is one of the biggest costs associated with owning a home. And it doesn’t help that inflation is causing premiums to surge further. But there are several ways for you to keep your home insurance rates at an affordable level. Here are some practical tips and strategies.

It also pays to be smart about what you claim. But you need to be aware of what your policy includes. Here are 10 things that your home insurance covers that you may find surprising.

CPI’s data shows how inflation can have a significant impact on your car insurance rates. That’s why you can benefit from these practical strategies designed to keep your car insurance low.

You can find out more cost-effective tips for bringing your premiums down in our guide to cheap car insurance in Canada.

Are you feeling the impact of the high cost of living in Canada? How does it impact your insurance purchases? Feel free to share your thoughts below.