This article was produced in partnership with Hagerty Insurance.

Desmond Devoy, of Insurance Business Canada, buckled up to find out more about Hagerty Insurance’s policy offerings for your classic cars.

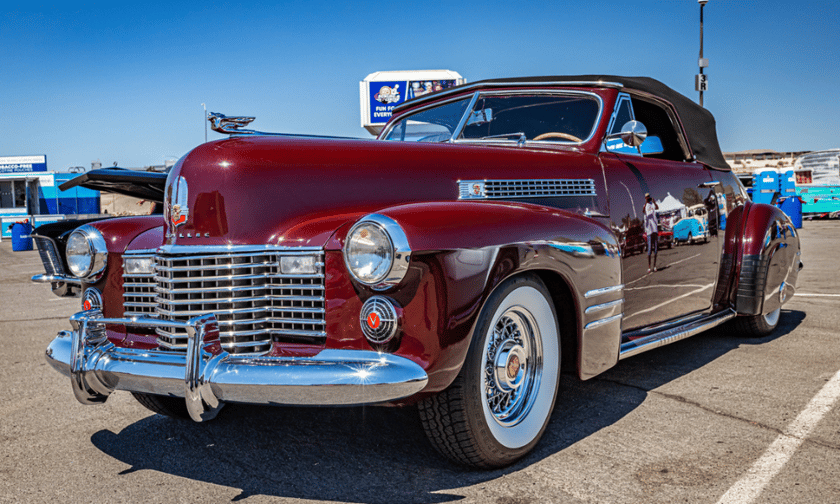

Your classic car is not a commuter car.

You don’t use your ’57 Chevy to get to work, or make house calls to clients in your ’68 Ford Mustang.

Your classic car is a pleasure to drive, and you drive it for pleasure.

Hagerty Insurance protects the vehicles people love, the vehicles that may be car show ready but are used for scenic drives and weekend road trips and car shows with gearhead buddies.

There are a few requirements for a client to qualify for a classic car insurance policy – and benefits beyond a lower premium and Guaranteed Value™.

The vehicle cannot be a daily driver and garage storage is preferred, though carports and driveways may also qualify in some provinces. Hagerty also considers vehicles that are under active restoration.

So, what can your car enthusiast client expect from a Hagerty Insurance classic car policy?

Up to $50,000 for new collector vehicle purchases.

Hagerty also offers additional coverages:

Now a 1908 Ford Model T is different than a 1990 K-Car, and Hagerty adjusts its coverage for collector vehicles accordingly.

Hagerty Insurance also has private client insurance, coverage for high-value vehicles and collections. Let’s say your client has a collection of more than six vehicles, valued at more than $250,000 (or one vehicle valued at more than $500,000.) This policy can offer enhanced services and protection, such as:

To your client, of course, their vehicle is priceless.

But, for all intents and purposes, you do need to put a price on that ride.

That’s why Hagerty has industry-leading tools to determine that classic’s true value.

Now what if there is a total loss?

In that case, your client will receive a cheque for the insured amount, guaranteed. *

No games. No hassle.

Plus, no appraisals are required on nearly all stock vehicles. (If Hagerty needs any further documentation in supporting the vehicle’s value, they will contact the owner during the underwriting process.)

How’s Guaranteed Value with Hagerty compare to competitors? Other insurers will typically pay total losses based on Actual Cash Value (ACV), an estimate of a vehicle’s fair market value, after considering factors like depreciation. They can also require an appraisal on the vehicle. Overall, this could mean a lower payout and a bigger headache.

The call of the open road is alluring, but sometimes you just need to get out on the water. Or get back to the land with your 1950s tractor. Remember our military history with a Korean War jeep? Or feel like you’re hunting ghosts in your “Ghostbusters”-like 1950s ambulance? Whatever your client’s collectible is, Hagerty has them covered:

For complete details regarding program eligibility, including annual mileage, driving record/experience and more, visit https://www.hagertybroker.ca?aff=prt_ins&utm_source=partner&utm_medium=referral&utm_campaign=ins_aut_ca&utm_content=article&utm_term=Insurance_Business_Canada_What_We_Protect_Article or call 888-349-7834.

(* Less any deductible; Manitoba and Saskatchewan: and after settlement with your government policy. Includes any applicable taxes unless prohibited by law. Alberta and Quebec: Agreed value applies under the Guaranteed Value Plus Endorsement.)