Health insurance is designed to help policyholders offset the exorbitant costs of medical treatment by covering a portion of their healthcare and hospital expenses. But with each country implementing different public healthcare systems, the level of coverage likewise varies.

In this part of our client education series, Insurance Business discusses how health insurance plans work in the four major regions we cover – the United States, Canada, the United Kingdom, and Australia. We will also explain the different policies available for citizens and the benefits these plans provide.

We encourage insurance agents and brokers to share this article with their clients to help them understand this essential form of coverage.

In 2010, the US enacted the Affordable Care Act (ACA), a comprehensive reform law aimed at reducing healthcare costs for families and ensuring that more Americans have access to health insurance. Under the ACA, patients who may be uninsured because of limited finances or pre-existing conditions can now secure affordable coverage through their state’s health insurance marketplace.

Through these health insurance marketplaces, Americans can choose from a range of coverages designed to meet different healthcare needs.

“Some types of plans restrict your provider choices or encourage you to get care from the plan’s network of doctors, hospitals, pharmacies, and other medical service providers,” according to the government’s health insurance exchange website HealthCare.gov. “Others pay a greater share of costs for providers outside the plan’s network.”

Here are some types of plans that people can access through these health insurance marketplaces:

This type of health insurance plan often limits coverage to care from doctors who work for or are contracted with the HMO. Policies generally do not cover out-of-network care except in an emergency. Plans may likewise require that a policyholder live or work in its service area to be eligible for coverage. HMOs typically provide integrated care and focus on prevention and wellness.

This is a managed care plan where services are covered only if the doctors, specialists, or hospitals are in the plan’s network – except in cases of emergency. This means that if a policyholder opts for an out-of-network provider, they will have to cover the full cost of treatment themselves.

In this kind of plan, policyholders pay less if they access doctors, hospitals, and other healthcare providers belonging to the plan’s network. POS coverage also requires the insured to get a referral from their primary care doctor for them to see a specialist.

This health plan allows policyholders to pay less for healthcare if they choose to get treatment from providers in the plan’s network. However, they can also access doctors, hospitals, and providers outside of the network without a referral for an additional cost.

HealthCare.gov added that US health insurance plans are offered in four categories based on how the costs are split between the policyholder and the insurer. Also referred to as the “metal tiers,” these plans are:

One of the changes the ACA has implemented is the standardization of insurance plan benefits in the country’s healthcare system. Before this, the benefits offered varied significantly depending on the insurance company and the type of policy. At present, US health insurance plans are required to cover these 10 “essential health benefits.”:

Birth control and breastfeeding coverage are also required benefits. Dental and eye care coverage for adults, meanwhile, are not considered essential benefits but are available as optional add-ons, along with medical management programs.

Health insurance premiums across the US cost an average of $456 monthly per person, according to the latest marketplace benchmark premiums from the Kaiser Family Foundation. This can be a steep price to pay for some American families.

For many employed individuals, this may not be a cause for concern as their employers cover about four-fifths of their health insurance costs. But those without access to company-sponsored coverage need to shop around for their own health plan and cover the full cost of premiums.

According to HealthCare.gov, health insurers can only account for five factors when determining premiums under the ACA. These are:

States can limit how much these factors affect insurance rates but are prohibited from using medical history and gender in calculating premiums.

“Insurance companies can’t charge women and men different prices for the same plan,” HealthCare.gov explained. “They also can’t take your current health or medical history into account. All health plans must cover treatment for pre-existing conditions from the day coverage starts.”

Health insurance providers in the US offer basic policies to individuals and businesses – along with other services that can include Medicaid and Medicare policies, long-term care insurance, dental coverage, and vision benefits. The top 10 health insurance companies in the country control almost two-thirds of the market.

Canada’s healthcare system is regarded as one of the best in the world, providing all citizens and permanent residents free access to emergency care and regular doctor visits. However, there are still certain services that Medicare – the country’s universal health coverage – does not cover, which Canadians need to pay for.

Canada has a publicly funded healthcare system that operates under the Canada Health Act (CHA). To be eligible to receive full federal cash contributions, each provincial and territorial health insurance plan needs to comply with the five pillars of the CHA, which stipulates the that policies must be:

“Health care is funded and administered primarily by the country’s 13 provinces and territories,” according to the Commonwealth Fund, a private non-profit group that supports independent research on health care issues and provides grants aimed at improving the country’s health system. “Each has its own insurance plan, and each receives cash assistance from the federal government on a per-capita basis.”

The organization added that while benefits and delivery approaches vary, all Canadian citizens and permanent residents receive “medically necessary hospital and physician services free at the point of use.”

However, not everything is covered by Medicare. These include:

Canadians need to pay out of pocket for these, so it is not surprising that, although not required, nearly 70% of Canadians have taken out supplemental private health coverage, according to the latest figures from the Canadian Life and Health Insurance Association (CLHIA). Of these, 90% were purchased through group plans.

Canadian Medicare covers many of the healthcare basics, including:

Each province and territory implement their own rules when it comes to health coverage, so the exclusions may vary. For the following items and services, private health insurance may be necessary for coverage, depending on where a person lives.

The latest available figures from the Canadian Institute for Health Information (CIHI) estimated the cost of private health insurance at $756 per year, which is equivalent to $63 monthly. The institute’s data also showed that the average Canadian paid out $902 in out-of-pocket health expenses, or slightly over $75 each month.

These numbers, however, were taken before COVID-19 shook not just Canada’s healthcare system but also that of the world, so the values might actually be higher at present. In addition, the figures above are mere estimates and the best way to get an accurate amount is to contact the health insurance companies directly.

Canada is home to about 130 private health insurance providers, serving a total of 27 million Canadians. These companies offer some of the best supplemental health coverage.

The UK has a publicly funded healthcare system, called the National Health Service (NHS), which everyone living in the country can access for free.

The NHS operates a residence-based model rather than an insurance-based system. This means that anyone living and working in the UK, even those on a temporary work visa, is entitled to free healthcare through the NHS.

The NHS offers a wide selection of services, from primary care to specialised treatments. These include:

But just like the public healthcare systems in other countries, the volume of people accessing the NHS has resulted in long waiting times. Because of this, UK citizens can opt to take out private health insurance, which enables them to access specialists more quickly and use better facilities.

Private health policies in the UK are designed to cover the cost of private treatment for acute conditions. This means most health plans provide coverage for short-term, curable medical issues, rather than chronic illnesses, which people tend to live with throughout their lifetimes.

There are several types of private health insurance that Brits can access. These include:

Taking out private health insurance yields the following benefits:

However, there are also drawbacks and disadvantages of private health insurance:

An analysis conducted by London-based personal finance website NimbleFins has found that the average cost of private health insurance in the UK is around £85 a month or £1,200 annually.

Just like in other regions, premium prices are impacted by a range of factors. These include the policyholder’s:

Despite having access to one of the best public healthcare systems in the world, Australians may still need to endure long waiting times for non-life-threatening procedures. And just like in Canada, they may also need to pay for certain services that the country’s universal health insurance, also called Medicare, does not cover.

This is the reason why the Australian government is encouraging citizens to take out private health insurance through tax incentives and premium rebates.

Private health insurance in Australia pays out for medical expenses that are not covered under the public healthcare system. It can also cover the cost of treatment in a private hospital or if one chooses to be treated as a private patient in a public hospital. Australians must purchase policies only from registered health insurers.

There are two main types of private health coverage:

Citizens and permanent residents in most states and territories can also secure ambulance cover, which includes emergency transport and medical care. The exceptions are Queensland and Tasmania, where the state governments provide automatic coverage for residents.

The country’s Department of Health listed four main advantages of taking out this type of coverage on its official website. These are:

Premium prices of private health cover in Australia are influenced by several factors. These include the cover type and tier, how many people a policy covers, and the policyholder’s age, income, and residence.

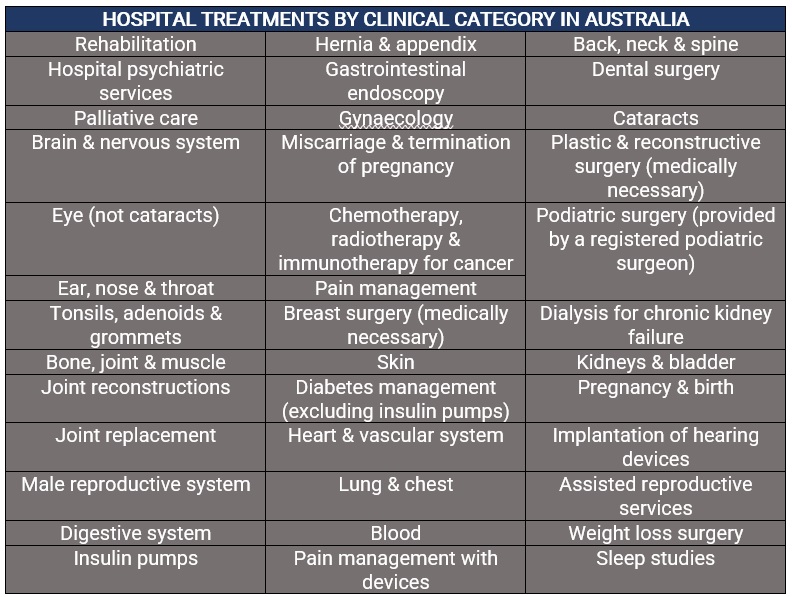

Hospital cover is available in four different tiers, namely Gold, Silver, Bronze, and Basic, each covering a mandated list of treatments. Because Gold policies cover all 38 types of treatments outlined by the government, they also come with the most expensive premiums.

An analysis by the comparison website Finder pegged the cost of a hospital cover for a gold policy at about $228 a month. Monthly premiums for basic, bronze, and silver policies are estimated to be $99, $120, and $180, respectively. For extra cover, the average is $68 per single policy per month.

Every year, the Private Health Insurance Ombudsman (PHIO) releases a State of the Health Funds report to provide both consumers and industry experts with comparative information on the performance and service delivery of all health insurers across the country. The report also ranks the top private health insurance providers in Australia based on a set of key indicators.

Is private health insurance something you are considering taking out? Is there anything you want to add that we might have missed? Share your thoughts in our comments section below.