Vehicles are an important part of many small businesses’ day-to-day operations. But not all businesses own the vehicles that they use. To keep your business financially protected when accidents occur, you need the right type of coverage.

Commercial auto insurance covers only vehicles registered under your business’ name. Your employees’ personal car insurance, meanwhile, don’t provide coverage for business-related incidents.

Enter hired and non-owned auto insurance. This type of policy protects your business if the vehicle that you rented or borrowed is involved in an accident. You can learn more about how this form of non-owned auto insurance works in this guide.

Hired and non-owned auto insurance, also referred to as HNOA, is a type of small business insurance that covers any vehicle that you rent, lease, or borrow for commercial purposes. This includes cars belonging to your employees.

Insurers don’t usually offer HNOA as standalone coverage. Instead, you can purchase it as a rider or endorsement for your commercial auto or general liability insurance, or as part of your business owner’s policy (BOP).

A hired and non-owned auto insurance policy provides protection mostly on a secondary basis according to Michael Schafer, area senior vice-president and casualty broker at Risk Placement Services.

“In most circumstances, if an employee gets into an accident [in their personal vehicle], their personal auto policy would be the primary policy in the claim,” Schafer explains. “So, if a pizza delivery driver gets into a fender bender, he would submit the claim to his personal auto insurer.

“Most companies that require employees to use their own vehicles will make their drivers contact their insurance agents to confirm if their personal auto policies will respond if they get into an accident in the course of doing business.”

Schafer adds that the limits on a personal car insurance policy are often “pretty small” compared to those in commercial auto insurance.

“Those limits can be exhausted quite quickly, and, in some cases, the insurance company might turn around and say: ‘Sorry, you were driving for X pizza delivery company at the time of the accident, so we’re not going to pick up this claim. You’re on their dime.’

“That’s where the HNOA policy would come into play – if a claimant named a company in a suit.”

HNOA policies are designed to compensate third parties. This means that you don’t need to pay a deductible. Depending on the circumstances surrounding an accident, your insurer covers the portion of the claims cost not covered by the primary policy. Compensation is given to the person who has filed the claim against your business.

HNOA acts as a form of liability car insurance. This means that it protects your business financially if you or your employees are legally responsible for an accident that results in another person’s injury, death, or property damage.

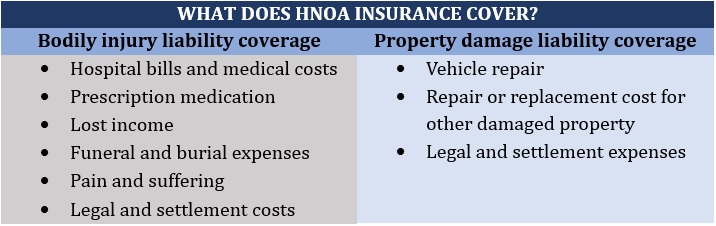

In general, hired and non-owned auto insurance provides two types of coverage:

This part of an HNOA policy pays for the cost to treat another person’s injuries because of an accident you or your employee has caused. It also covers legal expenses if your business is sued. Some policies provide compensation for lost time at work and a death benefit to cover funeral costs.

This type of HNOA coverage compensates another person for the damage and losses they incur due to an at-fault collision. It covers the cost of repairing or replacing their vehicle and other property and any legal and settlement expenses resulting from a lawsuit.

The table below sums up what a hired and non-owned car insurance policy typically covers.

HNOA covers two types of vehicles that you use for your business:

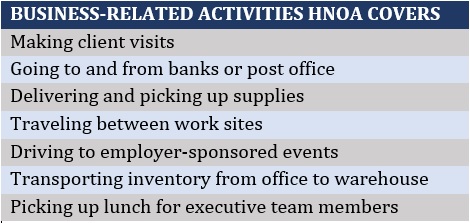

If you’re wondering what are considered business-related activities, you can check out some examples in the table below.

Hired and non-owned auto insurance provides coverage for all types of employees. These include all full-time, temporary, and volunteer staff.

Read more: Is getting non-owner car insurance worth it?

HNOA only provides third-party coverage for an at-fault accident. This means that the injuries that you and your staff suffer and any property damage to your businesses aren’t covered.

To be protected against these types of losses, you will need to purchase other forms of car insurance policies. Here’s a summary of what hired and non-owned auto insurance doesn’t cover.

HNOA won’t pay for the treatment and medical expenses that you and your staff incur, even if the accident isn’t your fault. To be covered, you will need medical payments (MedPay) or personal injury protection (PIP) coverage. PIP insurance is mandatory in no-fault states.

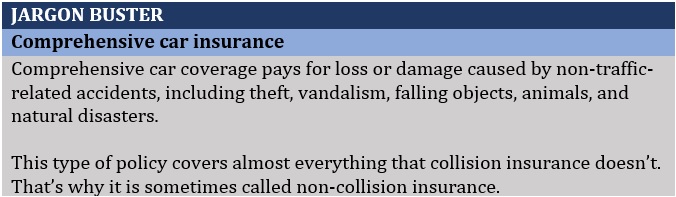

For vehicle damage, owners usually purchase collision and comprehensive car insurance policies. These combined with liability coverage comprise what is called full coverage car insurance. But this type of protection applies only if you own the vehicle. Luckily, if you have a commercial auto insurance policy, you can extend coverage to the vehicles you rent.

Non-owned auto insurance – collision car insurance definition

Non-owned auto insurance – comprehensive car insurance definition

Hit-and-run accidents are often covered under a commercial auto policy. For private vehicles, coverage is typically provided by uninsured motorist coverage, which is required in some states.

Your commercial property insurance should cover stolen items from your business, even if they’re outside the office premises, including hired vehicles. There are policies, however, that don’t cover theft committed by employees. For this, you may need to purchase a specialized type of rider for your business insurance, aptly called theft insurance.

No commercial auto insurance policy covers mechanical breakdown caused by normal wear and tear. You may need to self-insure for this one.

Each business comes with a unique share of risks, that’s why it is difficult to come up with a one-size-fits-all estimate of how much HNOA premiums cost. But based on the price comparison and insurer websites Insurance Business checked out, average premiums range between $120 and $170 monthly, or about $1,440 and $2,040 per year.

Just like other types of car insurance, the cost of HNOA depends on an assortment of factors. These include:

The coverage limits of your hired and non-owned auto insurance policy, as well as the amount of deductible you choose, also have a major impact on the premiums you need to pay.

The amount of hired and non-owned auto insurance coverage your business needs will depend on the unique risks it faces. A combined coverage limit of $300,000 to $500,000 for bodily injury and property damage often provides adequate protection for your business’ potential liabilities.

HNOA policies, however, cannot be purchased as standalone insurance. As it’s accessible primarily as a rider, it can push up the cost of your commercial auto insurance or business owner’s policy.

While your commercial auto coverage can be extended to rental vehicles, it doesn’t cover personal vehicles that your employees use for business-related tasks. Therefore, purchasing HNOA coverage to complement your commercial auto insurance policy is a smart move if you want extended protection.

If you own a small business that does the following, hired and non-owned auto insurance may be a worthwhile investment:

Another important consideration is your state’s minimum mandatory liability limits. While states don’t impose coverage limits for HNOA policies per se, this set of requirements may be a good starting point when working out an ideal policy limit.

Bear in mind that you will be responsible for paying out any expenses that exceed your liability coverage limits. So ideally, you will want to take out coverage beyond what these state requirements.

Minor fender-benders may not cost much, but sometimes it takes just one major incident to completely disrupt your business’ financial security. A single accident can get you on the hook for hundreds of thousands of dollars, that’s why it pays to have sufficient protection.

To find an HNOA policy that matches your needs, the first step is determining how much coverage you require. Ideally, your coverage limits must be enough to shield your business’ assets from potential lawsuits. Your HNOA policy also works together with your liability coverage to provide your business with adequate protection.

Hired and non-owned auto insurance, however, is just one of the many elements that make up your commercial auto and small business coverage. To ensure that your assets are fully protected, you may also need to take out other types of policies, depending on the nature of your business.

Getting the right coverage is an effective way of mitigating business losses. But this should also be paired with sound risk management practices to best protect your business’ finances and profitability.

Commercial car insurance is one way of protecting your company’s assets. But it’s not as straightforward as it seems. If you want to dig deeper into what kind of protection this type of coverage provides, our comprehensive guide to how car insurance works can prove useful.

Do you think hired and non-owned car insurance is a smart investment for businesses that use rental and borrowed vehicles? Share your thoughts in the comments section below.