Updated 10-24-2023

Fiduciary liability insurance, also known as management liability insurance, is intended to protect businesses and employers against claims resulting from a breach in fiduciary duty. Essentially, the policy protects parties against liability for managing or administering employee benefits plans.

In this article, Insurance Business answers all the pressing questions about one of the least understood insurance policies out there. If your business handles employee benefits plans and you want to learn more about this often-complex form of coverage, this guide can help you sift through the jargon. Read on and find out everything you need to know about fiduciary liability insurance.

Under the Employee Retirement Income Security Act of 1974 (ERISA), every individual included in an employee benefit plan document by name or title can be considered a fiduciary. This includes anyone with discretionary decision-making authority over the administration or management of the plan or its assets.

Common fiduciaries include:

“As a fiduciary, it’s your job to select advisors and investments, minimize expenses and follow plan documents exactly,” commercial P&C insurance giant Travelers explains in its fiduciary liability insurance primer. “You have a duty to act solely in the interest of plan participants and beneficiaries – not the company. That’s a lot of responsibility and it comes with potential liability that requires the right protection.”

A fiduciary works in the interest of a beneficiary, especially when an employee benefits plan under ERISA is involved. A fiduciary has the duty of acting in the interest of a principal or beneficiary. The fiduciary’s role is to provide their beneficiaries with some financial benefit.

The beneficiary, meanwhile, is the person or entity named in an employee benefits plan. As the name suggests, they are the ones who are set to benefit or receive compensation under the plan.

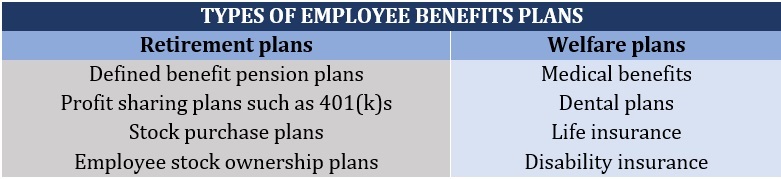

Employee benefits plans, which are managed and administered by fiduciaries, fall into two broad categories:

The table below lists some examples under these types of plans.

Life insurance is one of the most popular types of employee benefits plans. Learn more about how life insurance works in this comprehensive guide.

ERISA was passed in 1974 to ensure that employees participating in benefit plans, whether pension plans or welfare plans, get the benefits promised by such offerings. The law does not require employers to set up these plans for workers. Rather, it polices the plans once they’re put in place to ensure they meet certain standards.

The introduction of ERISA essentially created fiduciary liability exposures for employers that offer employee benefits plans. As a result of this, fiduciary liability insurance became widely available in the mid-1970s.

Any benefits plan covered by ERISA calls for fiduciaries or trustees to act exclusively in the interest of employees participating in the benefits plan, and their beneficiaries.

Other responsibilities include:

Fiduciary liability insurance will only cover the insured company and its employees engaged in fiduciary roles. The coverage doesn’t extend to third parties, outside advisers, or administrators of benefits plans.

“Any outside advisers, consultants, or administrators of your benefits plans … are responsible for securing their own coverage,” explains P&C and group benefits insurer The Hartford in its business owner’s playbook. “Also, keep in mind that even if you hire outside advisors to take on your plans’ fiduciary functions, this doesn’t automatically exclude you from any associated liabilities. You are still responsible for monitoring these fiduciaries’ activities.”

Fiduciary liability insurance protects fiduciaries against claims alleging:

Fiduciary liability insurance coverage works almost the same as professional liability insurance, which is called errors and omissions (E&O) insurance in certain industries.

Fiduciary liability insurance doesn’t cover a fiduciary who intentionally commits fraudulent acts. These include crimes that affect the benefits plan. Crimes are simply not covered by this type of insurance.

Apart from crimes like fraud, embezzlement, or theft, fiduciary liability coverage doesn’t cover mismanagement or failure to fund a benefits plan.

This type of insurance policy likewise doesn’t cover third-party fiduciary service providers in the event they mismanage the plan.

Any company that offers benefits plans has this exposure. While large organizations are more likely to have experienced personnel dedicated to employee benefits and well-versed in ERISA law, smaller companies may not. Therefore, smaller businesses might be more at risk of litigation.

Among the many forms of liability insurance that a company can have, very few are legally required. Fiduciary liability insurance is one of those not required by law.

While not mandatory, this type of insurance can be very useful, especially if a business decides to have or already has some form of benefits plan in place for their employees.

No, it’s not. Employee benefits liability insurance provides coverage for employee plan claims, but is limited to administrative errors, like failure to enroll. It doesn’t extend to breaches of fiduciary duty such as imprudent investment and so on. This coverage is normally an endorsement to a general liability policy.

Contrary to popular belief, ERISA bonds, employee benefits liability insurance, and to some extent directors’ and officers’ (D&O) insurance will not fully cover fiduciary exposures. That’s why fiduciary liability insurance plays a unique and vital role.

What is fiduciary liability insurance and why it's important for your plan. #Fiduciaryhttps://t.co/4iAcgijNIA

— EPIC Retirement Plan Services (@epic_rps) October 13, 2023

ERISA bonds are required under section 412(a) of the ERISA law. They’re different from fiduciary liability insurance.

This first-party coverage protects the plan and its participants by bonding any employee who handles funds or any other property of the plan. This protects the plan from risk of loss from fraud or dishonesty by the bonded employees.

While both types of insurance are concerned with retirement, benefits, or a health plan, their main difference lies in which party is covered.

ERISA liability insurance protects an employee benefits plan and its participants.

Fiduciary liability insurance, meanwhile, protects companies from liability while serving as the fiduciary or trustee of an employee benefits plan.

For example, if a business owner and their company put up a benefits plan for their employees, the business owner is considered a fiduciary. They must fulfill their fiduciary responsibilities as set by the US Department of Labor.

The business owner and certain employees are considered fiduciaries if they have authority over, advise, manage, or administer the plan.

Fiduciary liability insurance covers the fiduciaries and can cover claims arising from:

ERISA liability insurance covers the benefits plan and its participants.

Generally, this form of coverage requires that any employee who handles funds or other property attached to the benefits plan be bonded.

The bond that is used makes the fiduciaries personally liable, theoretically protecting the plan from risk of loss due to fraud or dishonesty on their part.

The type of bond that ERISA liability prescribes is a fidelity bond. Fidelity bonds are used to ensure that those bonded don’t incur losses from mismanagement, dishonesty, or acts of fraud.

A fidelity bond is specific to an individual. A surety bond, on the other hand, is specific to performing a job or executing a task, including fulfilling a contractual obligation and payment.

Simply put, a fidelity bond guarantees or covers a person while a surety bond ensures performance.

No. Fiduciary liability insurance provides coverage for risk or loss resulting from negligence, mismanagement, or errors. Intentional acts like fraud or theft causing loss to a benefits plan or its assets are not covered; that is the domain of a specific crime coverage policy.

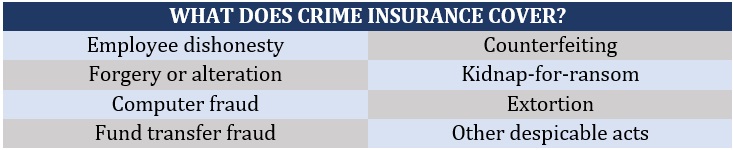

Crime coverage is an insurance policy against loss caused by fraudulent or willful criminal acts. The table below lists some examples of crimes covered under this type of policy.

Crime policies can cover a wide range of crimes committed by both employees and outsiders.

Yes. There are some insurance companies that offer crime coverage specifically for small and medium-sized businesses to mitigate risk or loss due to fraudulent acts.

Coverage can include:

Losses resulting from social engineering are also included and can come with a coverage of at least $100,000.

With the rapid shift to digital transformation, the insurance industry has also seen an upsurge in digital crimes. You can check out our cyber crime report tracker for the latest data breach and other cyber incidents involving insurance companies. Be sure to bookmark this page as it is updated regularly.

Yes. Fiduciary liability insurance is an excellent form of risk management. It protects the interests of your company and your employees. It is designed to protect a business from claims arising from mismanagement and liability from fiduciaries, such as errors and miscarriage of fiduciary duties.

Fiduciary liability insurance can also protect both the company and employees from fiduciary-related negligence, mismanagement, or any acts that can harm the plan participants.

That largely depends on whether your company offers any form of employee benefits plan. If your company is so small that it simply cannot afford to offer any benefits packages, then a fiduciary insurance policy is not necessary.

Once your company grows and decides to offer any sort of employee benefits, that’s when getting fiduciary liability insurance becomes a sound idea.

Although fiduciary liability insurance isn’t legally required when a company has a benefits plan, ERISA liability insurance is legally required by US labor laws.

To learn more about the different types of policies your business needs in challenging times, check out this comprehensive guide to business insurance.

Is fiduciary liability insurance a worthwhile investment? Do you have an experience where this type of coverage helped? We’d love to see your story in the comments section below.