5-Star Property 2022

Jump to winners | Jump to methodology

Weathering the storm

How do you make insurance more exciting? Take a booming housing market, mix it with environmental threats from climate change and flooding, add some inflationary pressures, and shake it up a bit. Voilà, you’ve got the market conditions for the commercial property insurance sector.

In the face of these interesting and complex forces, the winners of the 2022 IBC 5-Star Property awards have distinguished themselves as everything from office, retail, warehouse, and multifamily property insurers to providers of additional coverages such as flood and wildfire insurance, to MGAs delivering commercial and residential insurance – competently addressing the many needs of Canadians and their properties throughout the country.

“Given the way a number of foreign-based insurers have removed capacity from the Canadian market, a trend that continues with troubling impacts on brokers and customers, we believe it is more important than ever for Canadian property business to be placed with stable, reliable Canadian insurers”

Graham Haigh, Wawanesa

Challenging market conditions

Due to extreme weather events, rates have been high over the past few years, but fierce competition is helping rates to plateau or even soften.

One insurer that is keenly aware of the market conditions is Wawanesa, a winner in the multifamily property category of IBC’s 5-Star Property awards. The company’s senior vice president and chief marketing officer, Graham Haigh, says: “As a Canadian owned and operated mutual insurer, we are especially mindful of how the last few years in the property market have challenged our broker partners and our customers, especially keeping rates affordable.”

At Gore Mutual, a winner in the office category, Gavin Brown-Jowett, vice president of personal lines and underwriting transformation, also sees the pressure experienced by insurers in the personal property market. “Customers have a lot of choice and to win business, you must be constantly updating your offering and refining your rates. If you don’t offer a coverage that the rest of the industry does, you won’t win business. Conversely, if you have options that are unique and provide a value to customers, you can attract more than your share of business.”

One of the causes of the challenging conditions is severe weather. “While we are not seeing stronger claims ratios, which suggests the hard market is plateauing, we remain mindful of the cost of insurance and are increasing our focus on loss control, risk management and overall resiliency,” says Haigh.

Meanwhile, Cansure won in the MGA commercial property and MGA residential property categories. Their chief underwriting officer, Chris Marcinkiewicz, says the market has been softening after four years of positive hard market rate lift.

“Some classes of business – strata residential realty, for example – have showed definite signs of softening with a combination of rate and deductible reductions as fresh capacity entered this space in late 2021,” he says. “But the softening looks to be tempered overall with underwriters still able to get modest (<5%) rate increases overall.”

For the rest of 2022, Marcinkiewicz expects “competition on well-rated business to continue with further softening of the overall property market. We do see more aggressive pricing and competition in Eastern Canada, namely Ontario. Exposure to earthquake is holding overall rates for now in British Columbia.”

“If you don’t offer a coverage that the rest of the industry does — you won’t win business. Conversely, if you have options that are unique and provide a value to customers, you can attract more than your share of business”

Gavin Brown-Jowett, Gore Mutual

The flood factor

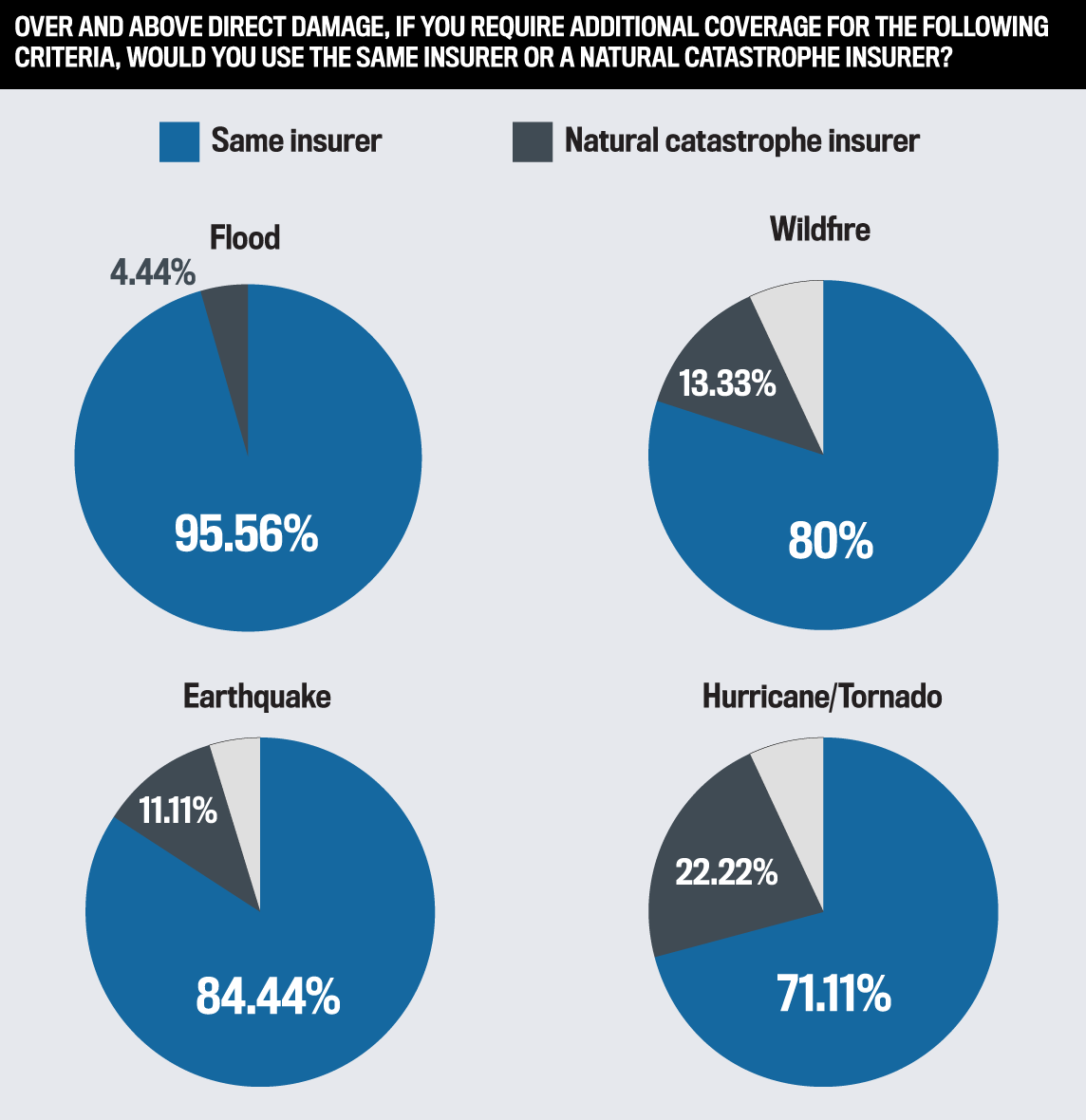

Flooding is now the number one cause of property damage in the country, with government figures placing the cost at over $1 billion per year. Over the past 10 years, floods have become an increasing concern in Canada. Extensive water damage has been caused by floods in Calgary, Southern Alberta, and Southern Ontario in 2013, the 2017 Quebec floods, and the catastrophic floods in British Columbia last year. The BC event was at least twice as likely to happen because of climate change, according to a study from Environment Canada.

Haigh says flood risk is a significant challenge for customers and society. “Prior to 2015, the only financial compensation available for overland flood damage to homes in Canada was the disaster financial assistance programs provided by the federal and provincial governments,” he says. “Today, Wawanesa and other insurers offer overland flood insurance across Canada.”

Brown-Jowett and Marcinkiewicz laud recent technologies as one of a few possible solutions.

“With the use of flood mapping tools, over the past number of years, insurers are now more selective in offering flood coverage to consumers,” says Brown-Jowett. “These types of losses occur in flood plains where coverage is not offered and uncommon. The Insurance Bureau of Canada (IBC) is working with the federal government on proposed solutions to the issue of flood coverage in areas prone to these losses.”

Meanwhile, Marcinkiewicz says: “Specifically regarding the commercial space, more accurate and broadly used flood modelling tools are being utilized by most domestic carriers, including ourselves. We’ve seen a combination of approaches being utilized such as ‘no write’ high flood zones, rate increases, higher flood deductibles and reduction is property capacity being deployed by carriers to offset flood exposure and attempt to maintain profitability in these flood-exposed areas while still offering coverage.”

“Going forward through 2022, we expect competition on well-rated business to continue with further softening of the overall property market expected”

Chris Marcinkiewicz, Cansure

Inflationary pressures on claims costs

Canadian insurers are all watching what’s happening in the United States, says Haigh, where they see a significant increase in claims costs because of inflation. “The impact of inflation on the severity of loss in Canada is just now starting to show, so we’re a bit behind, but we are watching closely.”

In March, inflation reached a more than 30-year high of 6.7%, with the property and casualty (P&C) sector running even higher. Homeowners’ replacement costs are up 13%. New vehicles are up more than 7%, used vehicles are up 34%, and rentals are up 24%, according to the IBC.

Meanwhile, Brown-Jowett and Marcinkiewicz have some figures of their own.

“Currently, inflation data shows inflation at 5.5% for combined labour and materials in construction, and 7.85% in restoration work,” says Brown-Jowett. “We feel that there will continue to be a rise in labour cost with labour shortages in the restoration industry contributing to the already consistent rise in labour rates over the past several years.”

While Marcinkiewicz says he estimates that inflation year to date has added more than 20% to the cost of claims. “Variables impacting inflation cost rise include: COVID labour shortages, rising fuel prices, rising materials costs, or an overall lack of material supply,” he says. “We estimate that this number could run to 30%-40% in the next six months. Of course, rising claim costs without commensurate rate rise will begin to challenge overall underwriting profitability.”

What makes the winners stand out?

Although Haigh, Brown-Jowett, and Marcinkiewicz represent just three of the 18 winning companies, they provide a unique window into what makes an IBC 5-Star Property winner tick – what differentiates them from the competition.

“We are a Canadian owned and operated mutual that exists for the sole purpose of looking after our customers, brokers, employees and communities,” says Haigh. “We live in the communities we insure and we are committed to serving Canadians – it’s been that way with Wawanesa for over 125 years.

“Given the way a number of foreign-based insurers have removed capacity from the Canadian market, a trend that continues with troubling impacts on brokers and customers, we believe it is more important than ever for Canadian property business to be placed with stable, reliable Canadian insurers. I’d argue there are no better broker partners in Canada than mutual insurance companies.”

Meanwhile, Brown-Jowett says Gore Mutual stands out by offering a standard P&C portfolio as well as coverage to fill gaps, such as standalone rental and seasonal property coverage. “With our Next Horizon strategic transformation, we continue to overhaul complicated systems and processes that our industry depends on today with a focus on creating a high-performing, scalable business model centered around innovative customer and partner experiences,” he says. “As a mid-size modern mutual, we can work closely with broker partners to find solutions for their customers. Customers are looking for an experience and association and we are modernizing the value proposition through purpose.”

Describing Cansure’s value proposition, Marcinkiewicz says: “We are a large niche and general market MGA with strong delegated underwriting authority and referral avenues into the largest insurers in Canada and Lloyd’s of London markets. Our differentiation from others stems from our broad product offerings in property, liability, specialty lines, commercial, personal, marine and inland product offerings. We consider ourselves a one-stop shop and being a ‘solution-first’ focused underwriting company.”

5-Star Property 2022

INSURANCE PROVIDERS

Care homes

- Intact Insurance

Office

- Aviva Canada

- Economical Insurance

- Gore Mutual Insurance Company

- Intact Insurance

- Northbridge Financial

Retail

- Aviva Canada

- Economical Insurance

- Intact Insurance

- Northbridge Financial

Industrial

- Aviva Canada

- CNA Insurance

- CHES Special Risk

- Intact Insurance

- Northbridge Financial

Warehouse

- Intact Insurance

- Northbridge Financial

Hotels and motels

- Aviva Canada

- CHES Special Risk

- Intact Insurance

Multi-family property

-

ABEX

ABEX

- Aviva Canada

- CHES Special Risk

- Economical Insurance

- Intact Insurance

- Wawanesa

Student housing

-

ABEX

- April Canada

- Cansure

- Intact Insurance

Shopping malls

- Aviva Canada

- Intact Insurance

- Travelers

Residential

- Aviva Canada

- Commonwell Mutual Insurance Group

- Gore Mutual Insurance Company

- Intact Insurance

- Wawanesa

ADDITIONAL COVERAGE

Floods

- Intact Insurance

- Lloyd’s

Wildfires

- Intact Insurance

- Lloyd’s

- Travelers

Earthquakes

- Lloyd’s

Hurricanes/Tornadoes

- Lloyd’s

MGAs

Commercial Property MGAs

-

ABEX

- April Canada

- Burns & Wilcox

- Cansure

- CHES Special Risk

- Premier

- Totten Group

Residential Property MGAs

-

ABEX

- April Canada

- Cansure

- CHES Special Risk

- Premier

- Totten Group

Methodology

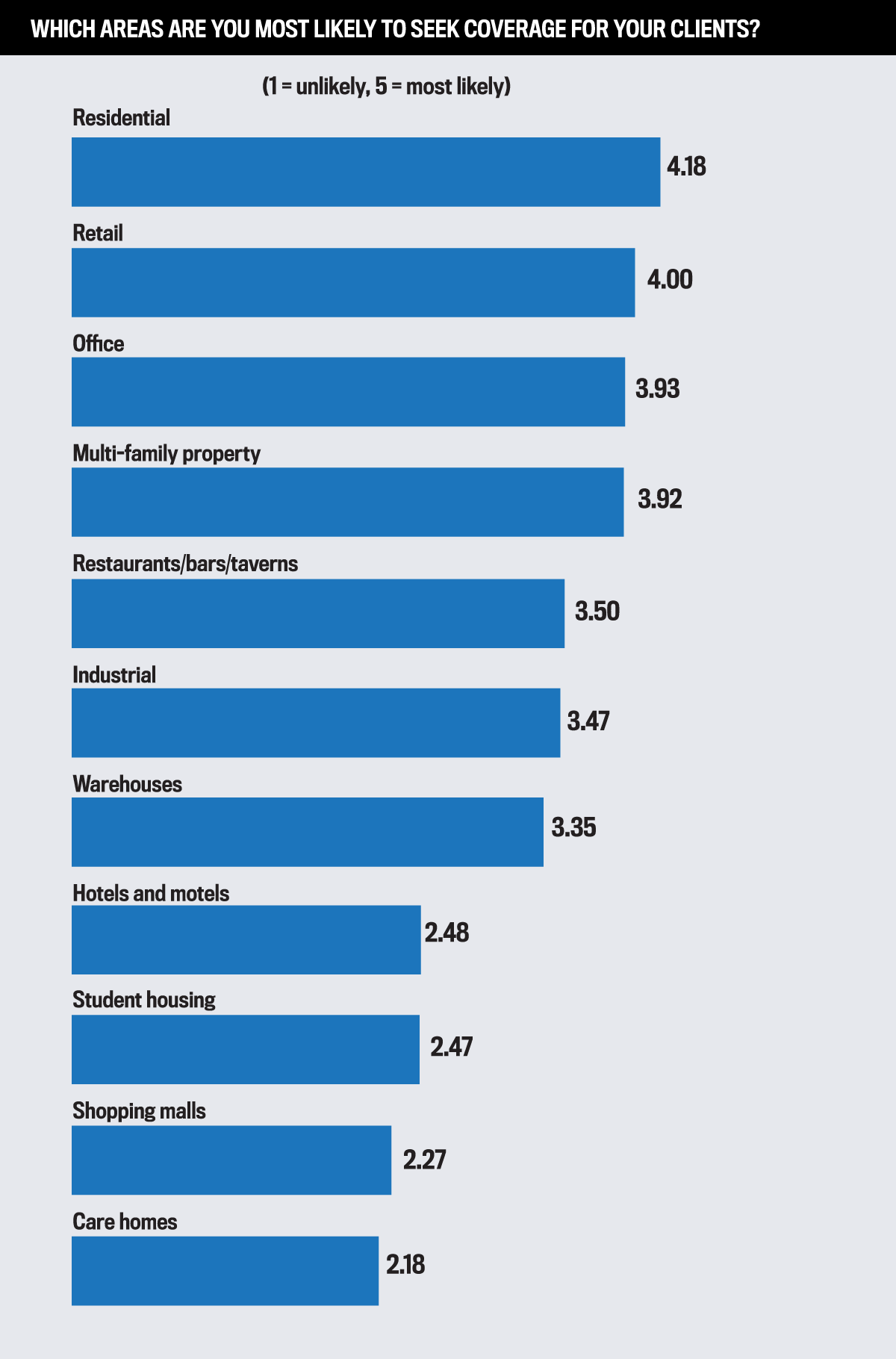

To uncover the best property insurance providers in the Canadian insurance industry, the Insurance Business team undertook a rigorous marketing and survey process, leveraging its connections to brokers across the country. Brokers were asked to nominate their property insurers and MGAs on a number of key areas: office, retail, industrial, warehouse, hotels and motels, multi-family property, care homes, student housing, shopping malls, and residential property. IBC also asked brokers which insurer they would use for additional coverage such as floods, fires, earthquakes, and hurricanes as well as their top choice of commercial and residential MGAs. The most voted property insurance providers were given 5-Star Property awards for 2022.

Keep up with the latest news and events

Join our mailing list, it’s free!