Flood risks are sending home insurance costs soaring by as much as 20% in some Ontario cities, according to a new report.

The joint study from digital broker MyChoice and real estate platform Wahi suggests that story missed a fast‑growing cost centre: home insurance in flood‑exposed communities.

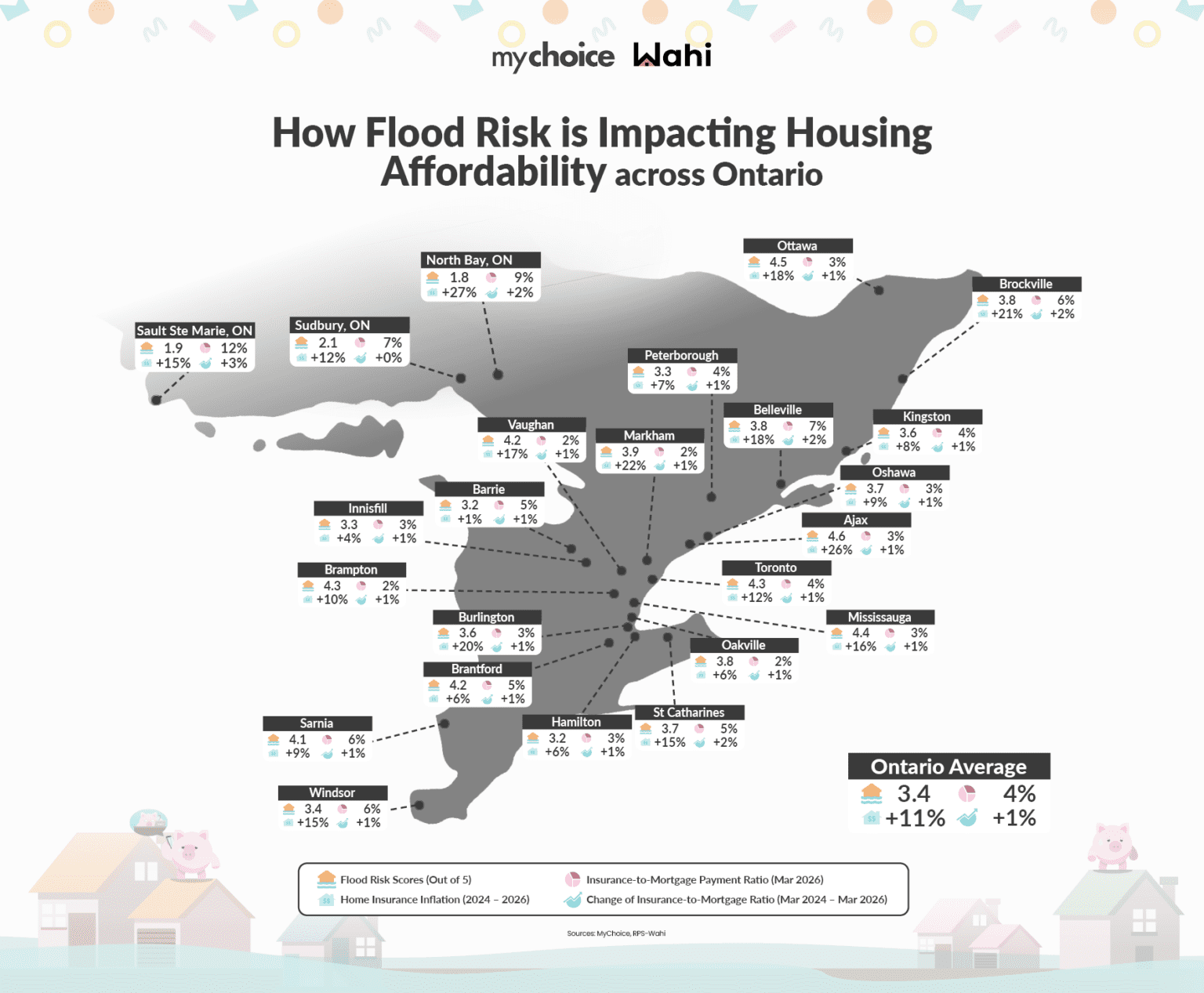

Drawing on insurance quotes and the RPS‑Wahi Home Price Index across 39 Ontario cities, the report compared 2024 and 2026 premiums using a standardized homeowner profile and a five‑year fixed mortgage with 20% down.

It found that in high‑risk urban markets such as Ajax – the study’s top‑ranked city for flood exposure – premiums jumped 26% to $1,290, even as they remained about 3% of a typical mortgage payment.

For now, though, the issue hasn't become a hot-button topic for mortgage brokers in their discussions with borrowers.

Jerry Liu, an Ajax-based broker with 8Twelve Mortgage, told Canadian Mortgage Professional clients didn't seem overly concerned, in their broker conversations at least, about the hike.

"This really hasn't been much of a topic of conversation between my clients and I," he said. "With a lot of first-time homebuyers, they aren't really too aware of the increased rate premiums year to year, since this is their first premium."

Thunder Bay posts the highest average premium in 2026 at $2,264, followed by Sudbury at $1,809 and Sault Ste. Marie at $1,791.

On the other hand, Kitchener has the lowest average premium at $1,021, with Ajax at $1,290 and Brockville at $1,288 among the least expensive on an absolute basis.

Those dollar amounts told only part of the story. In Thunder Bay, insurance accounts for about 11% of a typical mortgage payment, with North Bay around 9% and Sault Ste. Marie at 12%, the highest ratio in the province under the study’s assumptions.

By contrast, larger centres with higher home values, including Toronto, Mississauga and Ottawa, see insurance remain in the 3% to 4% range even as premiums climbed by double digits.

In Sarnia, where flood risk scores are elevated, insurance makes up about 6% of mortgage payments despite only single‑digit premium growth.

“Affordability isn’t just about what you pay for a home anymore, it’s increasingly about what it costs to protect it,” Aren Mirzaian, CEO of MyChoice, said.

“Rising home insurance rates in flood‑prone areas might be pushing potential home buyers our of those markets.”

Flash floods in Toronto and southern Ontario in July 2024 caused close to $1 billion in insured damage, one of the costliest flood events in Ontario’s history, industry estimates showed.

Nationally, severe weather pushed insured losses to a record $8.5 billion in 2024 and a further $2.4 billion in 2025, putting sustained pressure on property premiums.

Unlike the United States, which relied on the long‑running National Flood Insurance Program, Canada still does not have a fully implemented national flood insurance backstop. Ottawa signalled support in recent budgets, but as of 2026 federal officials have yet to commit to a launch timeline – an uncertainty that leaves more risk priced directly into private premiums.

Make sure to get all the latest news to your inbox on Canada’s mortgage and housing markets by signing up for our free daily newsletter here.