The rise in wildfire activity has prompted insurers to reassess exposure, especially in higher-risk zones, according to a wildfire risk analysis released by Canadian insurtech firm MyChoice.

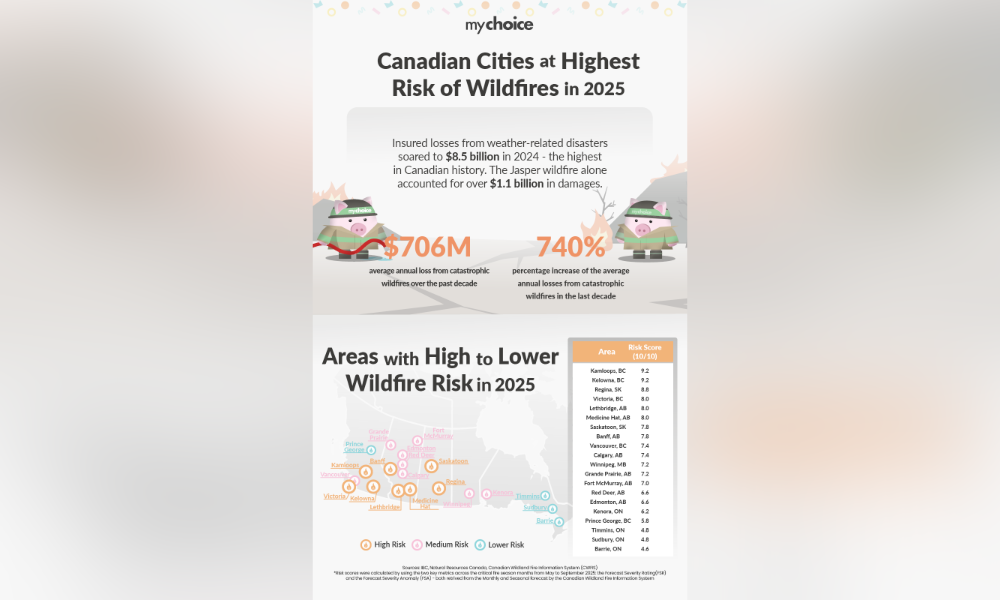

The 2025 wildfire season in Canada has begun with multiple fires in British Columbia, prompting partial evacuations in areas near Fort St. John. This follows a record-setting year in 2024, when insured losses from weather-related disasters reached $8.5 billion — the highest on record. The Jasper wildfire alone resulted in more than $1.1 billion in claims.

Over the past decade, average annual insured losses from catastrophic wildfires have risen to $706 million, up from $84 million in the previous decade, reflecting a significant increase in frequency and severity.

The report uses city-level wildfire risk scores based on the Forecast Severity Rating (FSR) and the Forecast Severity Anomaly (FSA), sourced from the Canadian Wildland Fire Information System. These metrics track predicted fire intensity and deviations from historical patterns between May and September. Each city’s score represents an average of its monthly FSR and FSA values.

Kamloops, BC, ranked highest with a score of 9.4 out of 10, up from 9.2 in 2024, driven by consistent high anomaly readings and fire conditions. Saskatoon, SK, followed with a score of 8.8, reflecting increased forecast severity in July and September.

Meanwhile, Kelowna, BC, remained at 8.6, the same as the previous year. Medicine Hat, AB, and Regina, SK, also scored 8.6. Grande Prairie, AB, and Lethbridge, AB, both posted scores of 8.4, showing a slight increase from 2024, while Fort McMurray, AB, rose from 7.0 to 8.0.

Winnipeg, MB, increased to 7.8, while Edmonton, AB, remained stable at 7.0. Prince George, BC, rose to 7.4 from 5.8 last year. Calgary, AB, dropped to 6.2, and Red Deer, AB, fell to 5.8. Cities in Ontario such as Timmins, Kenora, Sudbury, Barrie, Sault Ste. Marie, and Gravenhurst remained in the 5.2 to 5.4 range, showing minimal change.

While Canada’s insurance market has so far avoided the full-blown crisis seen in California amid its wildfires, the warning signs are clear. Canada’s open insurance market and competitive environment have helped maintain access to coverage, but signs of strain are emerging.

Aviva’s decision to withdraw its direct-to-consumer business from Alberta in early 2025 reflects early indicators of insurer retreat similar to trends in California. With annual wildfire losses in Canada rising from $84 million to $706 million over the past decade, and events like Jasper pushing losses above the billion-dollar mark, Canadian policymakers may no longer be able to treat the California experience as remote, according to MyChoice.

Reinsurance has also taken a more prominent role in 2025, serving as a financial buffer against large-scale loss events. Global reinsurer capital reached a record USD $715 billion in Q3 2024, an increase of $45 billion since the end of 2023, driven by asset recovery, retained earnings, and activity in the catastrophe bond market.

In Canada, where 2024 was the costliest year for catastrophe claims, most reinsurance programs were triggered. Reinsurers responded by tightening terms, with loss-affected programs seeing risk-adjusted rate increases between 10% and 40%.

Aren Mirzaian, CEO of MyChoice, addressed actions homeowners can take to mitigate risk. “After a year like 2024, where wildfire losses in Canada reached unprecedented levels, preparation is more important than ever,” said Mirzaian. “While insurers and reinsurers are adjusting to rising climate risks, homeowners can take practical steps to reduce their exposure. Clearing dry brush, trimming trees to maintain distance from the home, installing fire-resistant roofing and siding, and storing flammable materials away from structures can go a long way. Not only do these measures help protect your property, but they also strengthen your position when it comes to securing affordable insurance in high-risk areas.”