Updated: November 23, 2023

Mortgage default insurance is required by law if you’re purchasing a home with less than 20% down payment. It’s a necessary expense for many Canadian homebuyers.

But for something that’s so common, many remain in the dark about the true purpose of this form of coverage.

In this client education article, Insurance Business sheds light on how this type of policy works. We will discuss what it covers, who it protects, and the pros and cons of getting coverage.

We also encourage insurance professionals and lenders to share this guide with aspiring homeowners who may be seeking answers about this policy. Read on and find out everything you need to know about mortgage default insurance.

If you’re buying a home with a down payment of less than 20% of the property’s market price, there’s no way around it. You’re legally required to insure your mortgage in the form of mortgage default insurance.

Canadian law allows banks and other lenders to only provide financing to qualified homebuyers with at least a 20% down payment. That’s unless the mortgage is protected against default. This is what mortgage default insurance – also called mortgage insurance or CMHC insurance, named after one of the country’s largest mortgage insurers – is designed to do.

Many homebuyers consider mortgage insurance as a “necessary evil.” It’s something that you need to pay for to realize your homeownership dream faster.

One of the biggest misconceptions about mortgage default insurance is that it provides homebuyers with some level of financial cushion if they fail to make payments. The reality, however, is that this type of policy protects lenders if a borrower defaults on their mortgage.

If the homebuyer fails to meet repayments, the lender may take legal action to reclaim the borrowed sum. This includes selling the property. The insurer then compensates the lender should there be a shortfall after the home has been sold.

The defaulting borrower, however, remains responsible for any shortfall in the mortgage. This means that the mortgage insurer or lender may still pursue them for any deficiency after the sale of the property.

The lender decides where to get the insurance. Technically, the lender also pays for coverage, but the cost of those premiums – usually between 1% and 3% of the total loan value – is passed onto the borrower.

Currently, there are three mortgage default insurance providers in Canada. If you apply for a home loan with mortgage default insurance, your lender submits your application to one of these three providers for approval:

CMHC is the primary insurer for housing in small and rural communities. It is also the only insurer of mortgages for multi-unit residential properties. These include large rental buildings, student housing, and nursing and retirement homes. CMHC is the largest provider of mortgage default insurance in the country by far.

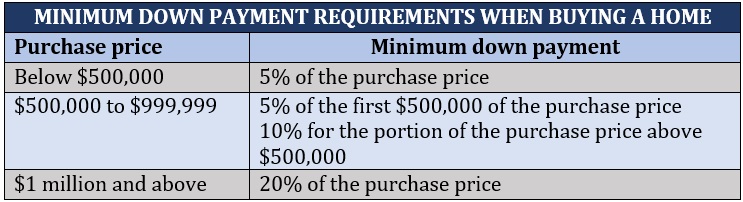

Saving enough for a down payment is often the biggest obstacle to homeownership. Ideally, you should have saved up at least 20% of the market value of the property you plan to buy to apply for a loan. However, this amount is often too high for many Canadian homebuyers to afford.

This is where mortgage default insurance comes into play. It allows you to purchase a home with a minimum of 5% down payment. Here’s how much you’ll need to shell out if you plan on buying a property.

The percentage of money you pay upfront as your down payment determines whether your mortgage is high or low risk, more commonly known as high ratio or low ratio.

If you have less than 20% as a down payment, then the mortgage is considered to have a high loan-to-value (LTV) ratio. This means that the ratio of the amount of the loan to the value of the property is high.

Conversely, if you have more than 20% down payment, the amount of the loan relative to the value you have in the property is lower. The lower the LTV ratio, the less risky your loan appears to your lender. If you have a high LTV ratio, it’s seen as a risky loan, requiring private mortgage insurance.

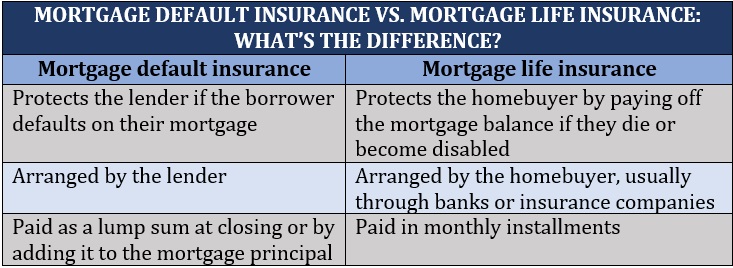

Because of their similar sounding names, mortgage default insurance is often confused with mortgage life insurance. But they’re entirely different policies.

While mortgage default insurance protects the lender financially if the borrower defaults on their payment, mortgage life insurance covers the homebuyer and their family. This type of policy pays off the mortgage balance if the homebuyer dies or become disabled.

And unlike mortgage default insurance, mortgage life insurance – also known as mortgage protection insurance – isn’t mandatory.

Here’s a summary of the key differences between the two policies:

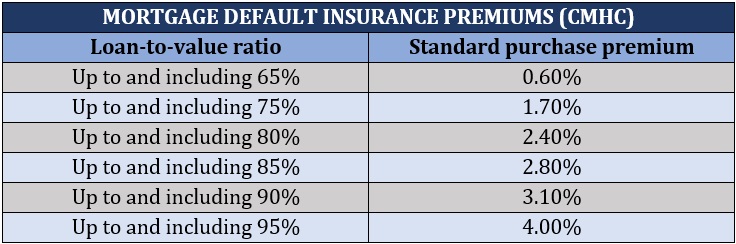

The insurer calculates mortgage default insurance premiums as a percentage of the loan principal amount. That percentage is based on the LTV ratio of your mortgage. The premium is generally rolled into the mortgage but can be paid upfront as part of the closing costs.

If the premium is added to the mortgage amount, then you will pay interest on the total amount borrowed, including the mortgage insurance premium. Premiums in Manitoba, Ontario, Saskatchewan, and Québec, however, are subject to provincial sales tax. This tax cannot be added to the loan amount and is due at closing.

Here’s an example of the premiums charged by the CMHC:

Using the figures above, if you purchased a $600,000 home with a 10% down payment, your purchase premium would be 3.1%. Calculated, your mortgage insurance premiums would be $16,740 (or $540,000 x 3.1%).

This CMHC mortgage insurance calculator from our sister publication Which Mortgage can also help you with the calculations. It’s important to note that standard purchase premiums vary depending on the insurer and lender.

Each insurer has its own eligibility criteria when it comes to mortgage default coverage. Your lender can apply for coverage if:

The CMHC also imposes these additional requirements:

As a borrower, you generally wouldn’t have any contact with the mortgage default insurance provider because your lender selects the mortgage insurer, not you. The insurer then decides whether a mortgage can be insured.

Because of this, it’s possible that your lender may approve your mortgage application, but the mortgage insurer won’t. In that case, you wouldn’t be able to get a mortgage unless your lender decides to try another insurer.

If you’re buying a home that’s worth more than $1 million, then that home is not eligible for mortgage insurance.

But even if you have more than 20% down payment, there are some circumstances when your lender may require you to get mortgage insurance. This would depend on the location and type of property.

If you are buying an investment property, that property wouldn’t be eligible for mortgage insurance. Because of this, you will need at least 20% down payment to buy one.

The amortization period of your loan also mustn’t exceed 25 years to qualify for coverage.

There are certain benefits and drawbacks to taking out mortgage default insurance. Here are some of them:

Apart from being federally required if you have less than 20% down payment, mortgage default insurance does have a benefit to the home buyer. If this type of policy didn’t exist, then lenders wouldn’t be able to offer competitive mortgage rates to borrowers who are getting high ratio mortgages.

Rather than assuming all the risk, lenders share the risk with mortgage insurers. So, although you’re paying mortgage insurance, you’re benefiting from paying less interest on the total mortgage amount.

Obviously, having as big of a down payment as possible is the best option if you’re buying a home. It ends up saving you money in the long run.

If you can’t wait to save all that cash – or don’t want to use all your available cash up front – then mortgage insurance can prove handy. It assures your lender that they’ll be taken care of should you not be able to afford your mortgage.

Get breaking news and keep abreast of the latest developments in mortgage default insurance, as well as other types of coverage, in our Property Insurance News section. Be sure to regularly visit and bookmark this page for the latest updates.

Do you think taking out mortgage default insurance is worth it? Do you have experience with this type of coverage that you want to share? Chat us up in the comments section below.