Richard Gurney, global head of construction at Marsh Specialty, outlines the lay of the land in the construction industry.

IBC: Marsh recently published a new report, Future of Construction: A Global Forecast for Construction to 2030. What does it reveal?

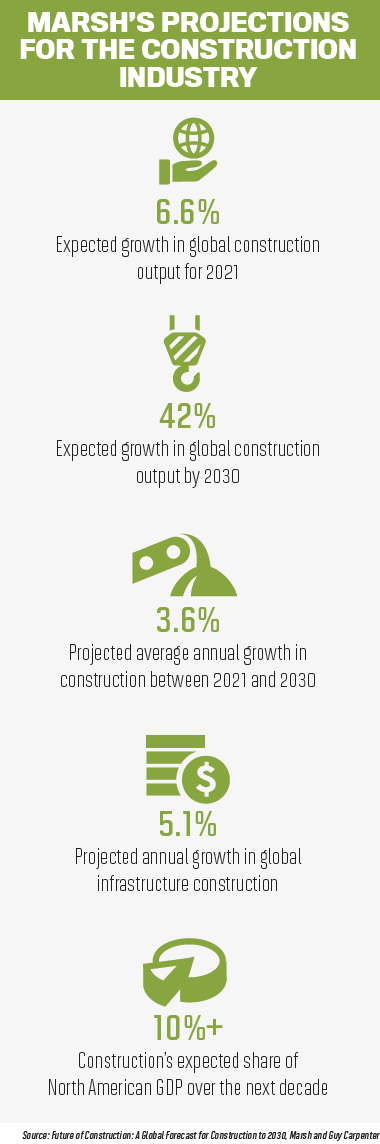

Richard Gurney: The fundamental finding underpinning it all is the level of growth we’re going to see over the next 10 years. From where we are now, we’re going to see 42% growth, which will take the industry to US$15.2 trillion. That’s huge in itself, but when you think about how it’s going to outstrip manufacturing and services, which is probably a surprise to some, it shows you just how significant construction is as a global industry.

We’re going through this phase where construction is used as a catalyst for post-pandemic stimulus. Construction is a very good way of getting capital into the system, but it’s going to move through in a phase of responding to population growth and urbanization and what’s going on regionally around the world. So, it’s an exciting time. That growth will outstrip what’s gone on in the last 10 years, and it will really be part of the bounce-back.

IBC: How has the construction industry been impacted by the COVID-19 pandemic?

RG: Initially, it proved incredibly resilient and nimble. But it’s important not to generalize, because if you look at the US, for example, it was far less interrupted than other parts of the world like Asia, where you’ve still got coun-tries that are, to a lesser or greater extent, in lockdown, and they’ve got projects that have stalled for 18 months or so. It’s not a homogeneous picture, but I think the industry proved itself incredibly resilient.

It learned quickly because it had to. Sites shut down, projects were delayed, contractors’ pipelines were delayed, and that all feeds into challenges around liquidity and free cash flow – so it was quite tough for contractors, particularly those that weren’t in the strongest position going into a completely unexpected event. But the business learned to adapt quickly, which is a real testament to it. And it looks now, with this next 10 years of apparent confidence and prosperity, to be in pretty good health.

IBC: How long-term do you think those impacts will be?

RG: We are currently going through a very inflationary cycle. There’s this sudden boom in the demand for construction post-pandemic, and stimulus and demand for growth everywhere, but you’ve also got materials, equipment, and people in the wrong place, so that has caused a bit of a bottleneck. While that will improve, and the supply of materials, equipment, and items for incorporation will become more available as the system gets back to normal, there will still be pressure on supply chains because underlying demand for construction will be high.

And of course, the industry is very reliant on supply chains – not just for materials, but for labour as well. That supply chain fragility that we’re seeing has, I think, caused a scrutiny between what is sourced globally and what is sourced locally. We’re not moving away from globalization altogether, but there will be a look again at whether materials can be sourced locally or inter-regionally rather than internationally.

IBC: Has the construction insurance market remained resilient throughout the pandemic?

IBC: Has the construction insurance market remained resilient throughout the pandemic?

RG: Obviously, there was scrutiny of succession of works clauses and that sort of thing. Insurers wanted to know that when sites were stopped and then started up again, there was rigour around that process, because it can be quite a risk-laden operation.

The pandemic also coincided with what was a tough market cycle anyway, and insurers were already in a fully transitioned market phase of pricing. They also had to deal with the COVID-related claims, and some of those are still going around the court process now, and they had to adapt to needing to provide ongoing cover at a time when capacity had dropped out to a great extent. So, it was a challenge – but the market rose to it.